AI-Powered Digital Account Opening in 2026: Smarter KYC

In 2025 and 2026, onboarding is no longer a simple compliance step that happens before a customer can access financial services. It has become the first real trust decision that a bank, insurer, or fintech makes in a digital environment. At the same time, it is the first moment when customers decide whether a brand feels secure, efficient, and easy to work with. This is why AI-powered digital account opening has moved from being an innovation project to becoming a core business capability.

Why AI-Powered Digital Account Opening Matters in 2025 and 2026

Customer expectations have changed dramatically over the past few years. People now expect fast, mobile-first, and low-friction onboarding experiences that feel as seamless as the rest of their digital lives. Yet many financial institutions still operate with identity verification models designed for a physical, document-based world. This gap between digital experience and legacy trust systems is creating serious problems for conversion, fraud prevention, and operational efficiency.

AI-powered digital account opening helps close that gap by transforming onboarding into a real-time decision process. Instead of relying only on static document checks, organizations can use AI to analyze multiple signals at once and make faster, more accurate decisions. This allows them to improve customer experience without ignoring risk.

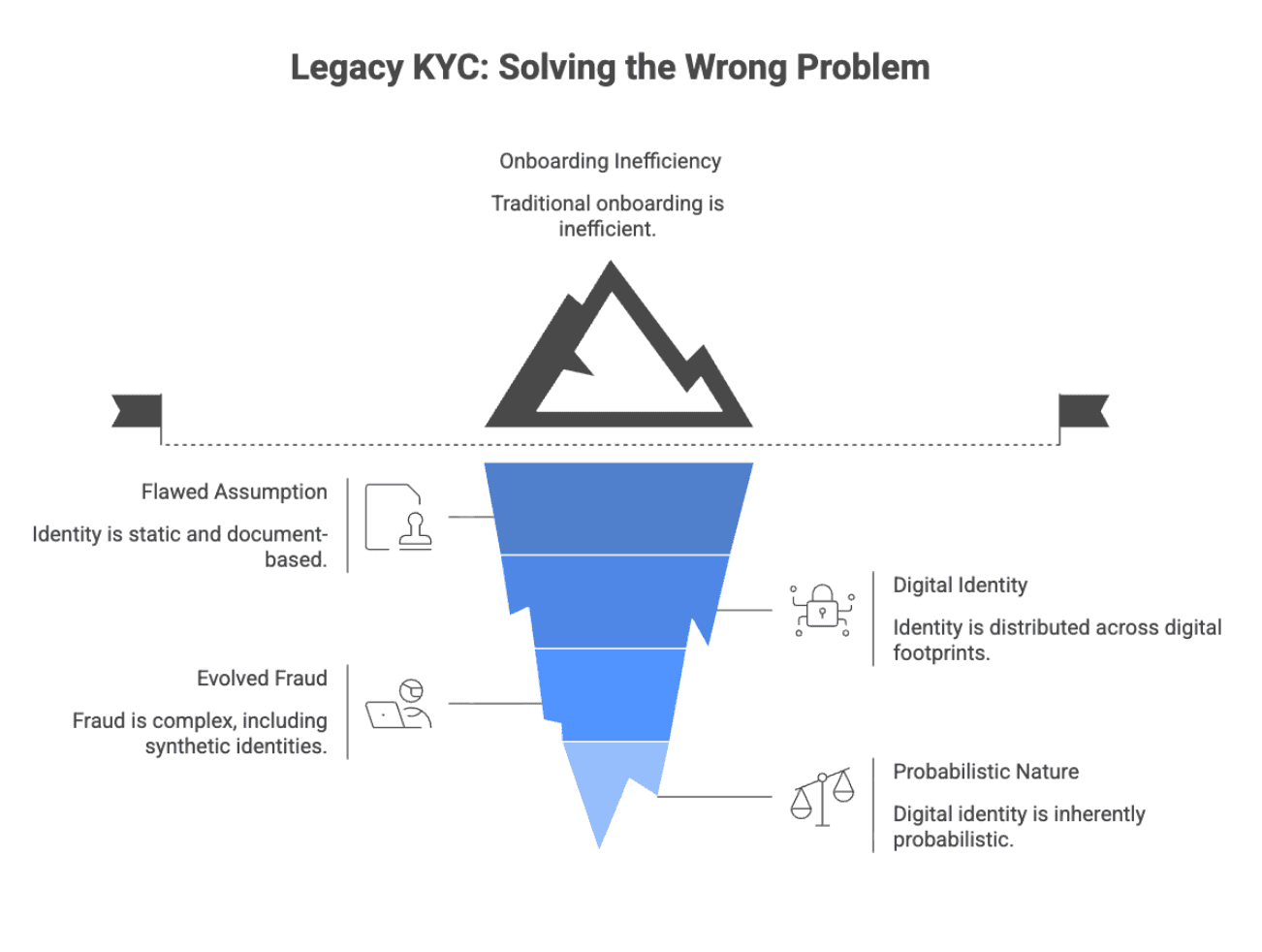

The Problem With Traditional Identity Verification

Traditional KYC processes were built on the idea that identity is fixed and can be confirmed through official documents. That model made sense when onboarding happened face to face and paper credentials were the primary source of trust. In today’s digital economy, that assumption is no longer strong enough.

Identity is now shaped by much more than a single government-issued document. It is reflected in behavior, device usage, location patterns, digital footprints, and session context. At the same time, fraud is becoming more advanced. Attackers are no longer limited to forged documents. They can now create synthetic identities, combine real and fake data, and even use generative AI to build highly convincing digital personas. The real weakness of legacy onboarding is not just that it is slow. It is that it is solving the wrong version of the identity problem.

AI-Powered Digital Account Opening and the Shift to Probabilistic Trust

One of the most important changes in modern onboarding is the move from rule-based verification to probabilistic trust modeling. Older systems are based on simple logic. If the information matches a fixed set of rules, the application is approved. If it does not, it is rejected or sent for manual review. While this approach is straightforward, it is too rigid for modern digital risk.

AI-powered digital account opening introduces a more adaptive model. Instead of asking whether an identity is either valid or invalid, AI systems assess how confident the institution should be in that identity at a specific moment. They combine biometric checks, data consistency, behavioral signals, device intelligence, and contextual information to generate a risk-based trust score. This creates a more realistic approach to digital identity, where trust is not absolute but measured on a spectrum.

AI-Powered Digital Account Opening Uses More Than Documents

Document verification and facial recognition still play an important role in onboarding, but they are no longer enough on their own. As AI-generated images, fake videos, and manipulated credentials become more common, static verification methods are losing reliability. A document may look authentic, and a face may appear real, yet the overall interaction can still indicate fraud.

That is why modern onboarding systems increasingly rely on layered identity intelligence. Behavioral biometrics, typing rhythm, interaction speed, device reputation, geolocation patterns, and session anomalies help create a deeper picture of authenticity. AI-powered digital account opening is effective because it treats identity as something dynamic and contextual rather than something proven once and forgotten.

AI-Powered Digital Account Opening Creates a Smarter Decision Layer

Many businesses focus too heavily on individual technologies such as OCR, facial recognition, or liveness detection. These tools matter, but they are not where the real competitive advantage is created. The real strength lies in the decision layer, where all signals are connected and translated into action.

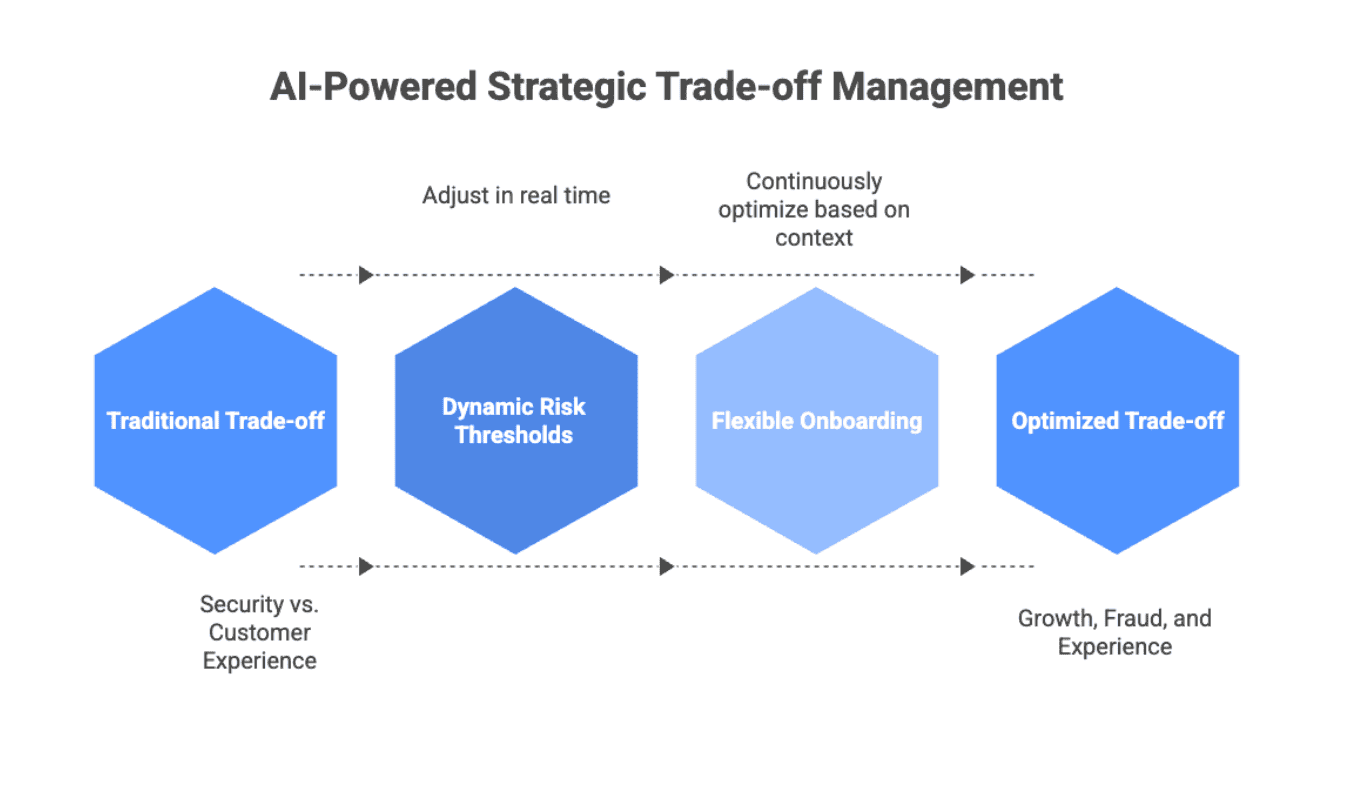

In advanced onboarding systems, AI does not simply detect risk. It helps institutions manage trade-offs in real time. A low-risk customer can move through onboarding quickly with minimal friction, while a higher-risk case can be escalated for additional checks. This ability to orchestrate signals and adjust thresholds dynamically is what turns AI-powered digital account opening into a strategic capability. It is not only about automation. It is about making better business decisions at scale.

Balancing Growth, Fraud, and Customer Experience

Digital onboarding is no longer a simple balance between security and convenience. In 2026, institutions must optimize three goals at the same time: growth, fraud prevention, and customer experience. That is much harder than it sounds. A fast onboarding journey may improve conversion rates, but it can also open the door to more fraud. A strict verification process may reduce fraud exposure, but it can also create friction and increase abandonment.

AI helps organizations manage this challenge more intelligently. Rather than applying the same controls to every applicant, institutions can calibrate onboarding based on customer type, risk profile, and real-time context. This makes the process more flexible and more commercially effective. AI-powered digital account opening does not remove trade-offs completely, but it allows institutions to manage them with greater precision.

AI-Powered Digital Account Opening Must Be Built for Compliance

As AI becomes more deeply embedded in identity verification, regulation is becoming more demanding. Institutions must now think more carefully about biometric data, explainability, auditability, governance, and cross-border data handling. These issues can no longer be addressed after the system is deployed. They need to be built into the design from the start.

This is why leading organizations treat compliance as a design principle rather than a final checkpoint. When transparency and governance are embedded into AI-powered digital account opening, institutions are better positioned to scale their onboarding model safely and sustainably. In this environment, compliance is not just a limitation. It is part of the foundation for long-term trust.

AI-Native Fraud Is Changing the Onboarding Landscape

Fraud has entered a new phase. By 2026, attackers are increasingly using AI to automate and scale identity fraud. Synthetic identities can be generated more convincingly, fake histories can be assembled more quickly, and biometric deception can be executed with far less effort than before. This changes the threat landscape in a fundamental way.

Organizations can no longer rely on static, rule-based defenses to keep up. They need systems that can learn continuously, detect emerging attack patterns, and respond in near real time. AI-powered digital account opening is becoming essential not only because it improves efficiency, but because it gives institutions a better chance to compete in an environment where fraud is also powered by AI.

AI-Powered Digital Account Opening Requires an Operating Model Shift

Adopting AI in onboarding is not just a matter of installing new software. It requires a broader transformation in how the organization works. Risk teams, compliance teams, product teams, and data teams must collaborate more closely than before. Leadership also needs a stronger understanding of how AI decisions are made, monitored, and governed.

This is why successful onboarding transformation is as much about organizational readiness as it is about technology. AI-powered digital account opening should be treated as a core operational capability, supported by strong data governance, aligned decision-making, and continuous model improvement. Without that foundation, even advanced tools will struggle to create lasting value.

From Onboarding to a Continuous Trust Lifecycle

The future of onboarding is moving beyond a single entry-point verification process. More institutions are shifting toward a continuous trust model, where identity is evaluated across the full customer lifecycle rather than only at account opening. In this model, onboarding becomes the first calibration point in an ongoing relationship of trust.

This shift supports new approaches such as continuous authentication, embedded onboarding, and identity-as-a-service. It reflects a broader reality of the digital economy: trust is no longer static. It must be recalculated as conditions change, risks evolve, and customer behavior develops over time. AI-powered digital account opening is the starting point for that broader trust architecture.

Conclusion

AI is not simply making onboarding faster. It is forcing institutions to rethink what identity, trust, and customer verification really mean in a digital-first world. The old assumption that trust can be established once through a document check is no longer enough. Identity has become more fluid, fraud has become more intelligent, and onboarding has become far more strategic.

In 2025 and 2026, the organizations that lead will not be the ones that adopt AI the fastest in isolation. They will be the ones that build AI-powered digital account opening into a smarter, adaptive, and continuously learning trust system. That is where stronger customer experience, better fraud control, and sustainable competitive advantage come together.