IT Insourcing vs. Outsourcing for APAC Banks: A Strategic Decision Framework for 2026

For more than two decades, outsourcing was one of the defining operating models of enterprise banking technology. It modernized core systems, expanded digital channels, and gave institutions across Asia-Pacific access to delivery capacity they couldn't have built internally on a reasonable timeline. For a great many projects, it still works exactly as intended.

The question facing an Australian CDO or a Singapore CTO in 2026 isn't whether outsourcing works. It's whether the traditional outsourcing model - a vendor that owns its own methodology, its own subcontractor chain, and the institutional knowledge generated along the way, is still the right structure for the work that actually matters: AI-enabled platforms under continuous development, sitting inside a regulatory perimeter that has tightened sharply in the past eighteen months.

The question facing an Australian CDO or a Singapore CTO in 2026 isn't whether outsourcing works. It's whether the traditional outsourcing model - a vendor that owns its own methodology, its own subcontractor chain, and the institutional knowledge generated along the way, is still the right structure for the work that actually matters: AI-enabled platforms under continuous development, sitting inside a regulatory perimeter that has tightened sharply in the past eighteen months.

That context has shifted on three fronts simultaneously. Artificial intelligence is moving from pilot to production inside core banking workflows, and production AI doesn't behave like a finished software project, it requires ongoing monitoring, retraining, and governance for as long as it's live. APRA's CPS 230 and MAS's evolving third-party risk regime have both made clear that accountability for a critical function never leaves the regulated entity, no matter how delivery is structured. And the cost of onshore engineering talent in Australia and Singapore has moved in one direction up at the same time AI-skilled engineers have become the scarcest, most expensive segment of the labor market.

Under those conditions, the binary "build it ourselves or outsource it" question stops being useful. What's emerged instead and what this framework is built around, is a third operating model: embedded insourcing, where a bank sources engineering talent from a market with a structurally better cost and supply position, but keeps that talent operating entirely inside its own governance, architecture, and product organization. The distinction isn't academic. It's the difference between buying delivery capacity and building delivery capability, and in a regulated, AI-driven environment, only one of those compounds in value over time.

The Insourcing Model, Explained: Embedded Teams vs Outsourcing in Banking

"Insourcing" gets used loosely in vendor marketing, so it's worth being precise about what actually changes operationally relative to the two models either side of it.

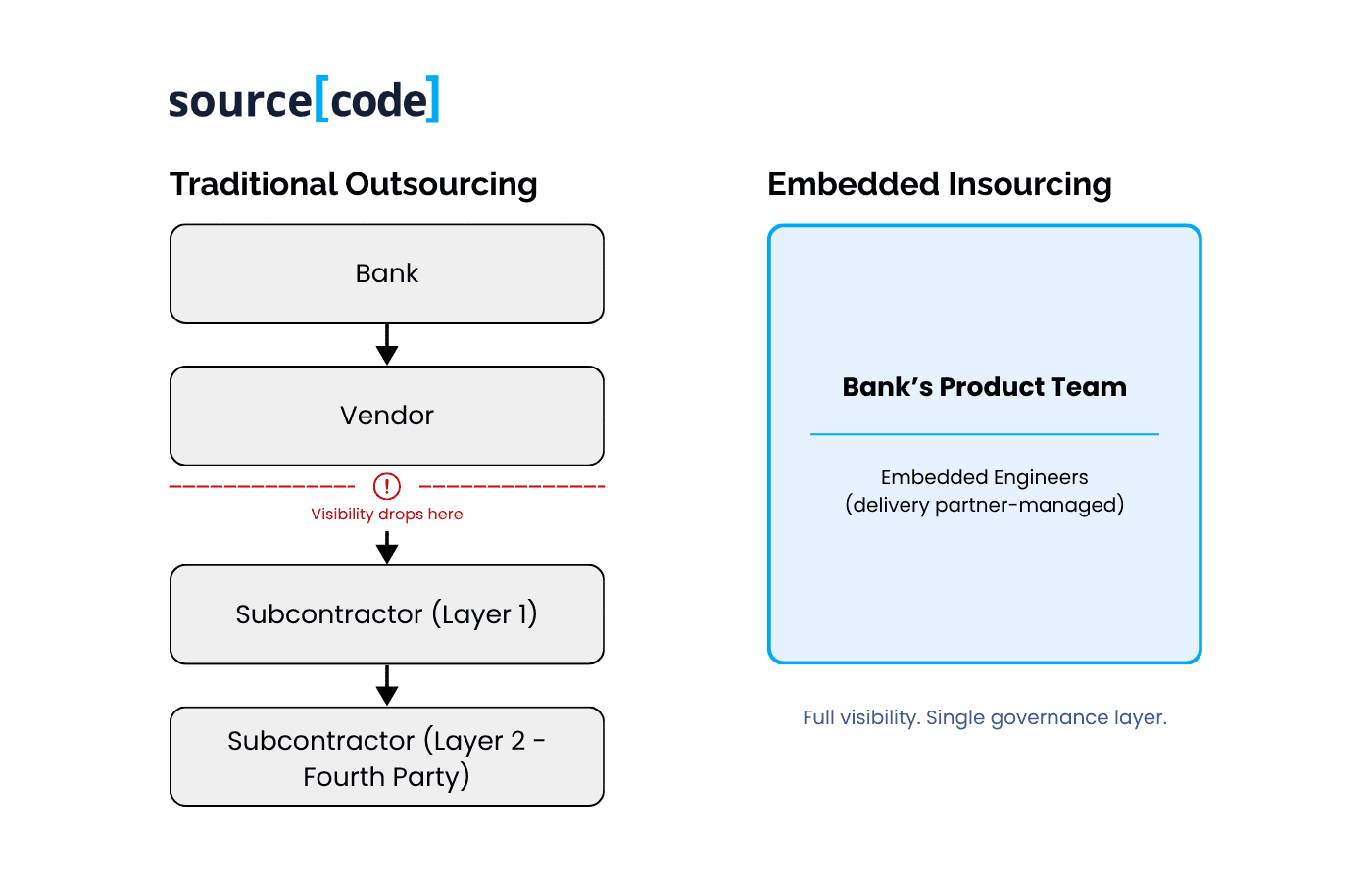

Traditional outsourcing transfers a unit of work: a project, a managed service, a ticket queue to a third party that owns its own delivery methodology, tooling, management layer, and frequently its own subcontractor chain. The bank buys an outcome or an SLA and has limited visibility into how it's produced. The vendor's commercial incentive is utilization and margin on the engagement; the bank's incentive is throughput and risk control. Those incentives aren't naturally aligned, which is why outsourcing relationships tend to accumulate friction at renewal and why, structurally, software gets delivered, but engineering capability rarely transfers back to the client.

Embedded insourcing inverts that. It brings the capability inside the bank's own operating model while sourcing the people from a market with a more favorable cost and talent structure. Engineers sit inside the bank's own sprints, use the bank's own tooling and repositories, report through the bank's own engineering leadership, and are subject to the bank's own security and change-management controls. They participate in product planning rather than simply receiving requirements handed down through a statement of work. They happen to be employed and operationally managed by a delivery partner in a market like Vietnam rather than recruited directly in Sydney or Singapore, but from a governance and architecture standpoint, they function as your own team.

In broader software delivery markets, this structure is often referred to as a dedicated team model or dedicated development team engagement - a stable, long-term pod of engineers aligned exclusively to your product, distinct from both project outsourcing (which transfers delivery ownership) and staff augmentation (which adds individual contractors temporarily). Within regulated financial services, the model carries additional shape: the compliance, governance, and audit obligations imposed by CPS 230 and MAS mean that a genuine dedicated team engagement must integrate into the bank's own control environment, not just its sprint cadence. That integration is what separates embedded insourcing from offshore staffing arrangements that borrow the same vocabulary.

The practical test that separates a genuine insourcing arrangement from relabeled staff augmentation is simple: who owns the architecture decisions, and who retains the institutional knowledge when the engagement evolves? In embedded insourcing, both stay with the bank, compounding with every sprint. In traditional outsourcing, both can walk out the door at renewal, which is precisely the failure mode APRA and MAS have spent the past two years writing rules to close.

Why Outsourcing Falls Short for APAC Banks Under CPS 230 and MAS Rules

Outsourcing isn't inherently flawed, it's mismatched to two specific categories of work that now dominate banking technology roadmaps: anything touching a critical operation under prudential regulation, and anything involving AI systems that don't stop evolving once they're "delivered."

AI doesn't fit into a project-shaped contract. A model that scores credit risk or detects fraud needs continuous monitoring, periodic retraining, drift detection, explainability testing, and governance sign-off for the entire time it's in production, not a one-off implementation milestone. That obligation doesn't end when a vendor's statement of work closes; it becomes a permanent operational responsibility. Project-based outsourcing, structured around fixed scopes and handover dates, is the wrong shape for a capability that needs to live inside the bank indefinitely.

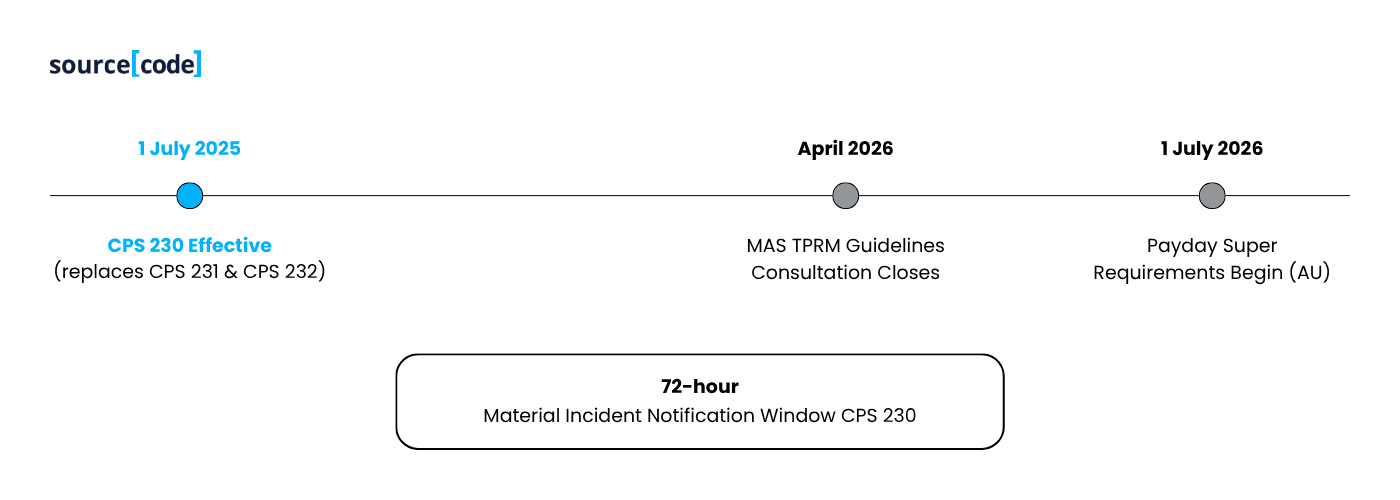

**Set-and-forget governance is a documented regulatory failure pattern. **The consequences of inadequate outsourcing oversight have moved from theoretical to enforcement-level. In mid-2025, APRA imposed additional license conditions on HESTA - one of Australia's largest superannuation funds, with approximately AUD 100 billion under management, after finding the fund was not adequately prepared to oversee a transition to an outsourced administration provider. The result was a disruption severe enough to leave over a million members unable to access their funds for weeks. APRA's conclusion was explicit: outsourcing does not remove a trustee's responsibility. That principle applies equally across banking, insurance, and superannuation. APRA's System Risk Outlook, published in November 2025, further signaled that the regulator is now actively collecting data on material service providers to understand concentration risk and cross-institutional dependencies, a direct signal that third-party oversight will intensify, not ease, going forward. CPS 230 - APRA's cross-industry standard that came into force on 1 July 2025, replacing the former CPS 231 (Outsourcing) and CPS 232 (Business Continuity), was built specifically to close this governance gap, with board-level accountability for operational resilience and a mandatory 72-hour notification window for material incidents.

The fourth-party blind spot. A bank can audit its direct vendor. It's far harder to audit the subcontractors that vendor relies on, staffing layers, sub-contracted delivery centers, cloud dependencies, several steps removed from the signed contract. CPS 230 explicitly extends obligations to these fourth-party relationships, requiring entities to identify and manage risk arising from the providers their material service providers themselves depend on. Multi-layered outsourcing arrangements make that visibility almost impossible to maintain with confidence and impossible to evidence to a regulator on demand.

The fourth-party blind spot. A bank can audit its direct vendor. It's far harder to audit the subcontractors that vendor relies on, staffing layers, sub-contracted delivery centers, cloud dependencies, several steps removed from the signed contract. CPS 230 explicitly extends obligations to these fourth-party relationships, requiring entities to identify and manage risk arising from the providers their material service providers themselves depend on. Multi-layered outsourcing arrangements make that visibility almost impossible to maintain with confidence and impossible to evidence to a regulator on demand.

Knowledge leaves with the contract. Outsourced delivery is priced and staffed around the engagement, not the codebase. When a renewal falls through or a vendor reallocates senior talent to a higher-margin account, the bank doesn't just lose capacity, it loses the people who understood why a particular control or architectural decision was built the way it was. That's a resilience problem, not a continuity inconvenience, and it's now a recognized feature of both APRA's and MAS's supervisory concerns.

Singapore's regulatory direction tells the same story. MAS's existing Notices 658 and 1121 already place direct, non-delegable obligations on banks for outsourced relevant services. MAS has since gone further: its proposed Guidelines on Third-Party Risk Management, consulted on through April 2026, extend obligations beyond formally defined outsourcing arrangements to any third-party relationship a financial institution relies on, regardless of contractual structure. The message from regulators in both jurisdictions is consistent and explicit: accountability cannot be outsourced. Only execution can.

Cost Comparison: AU Onshore vs APAC Insourcing Costs (With 2026 Data)

For years, sourcing decisions were dominated by a single metric: the day rate. If capacity could be bought more cheaply without visibly compromising delivery, outsourcing was the economically rational choice. That framing is now too thin for the decisions a 2026 CDO or CTO actually has to make, but the underlying cost data still matters enormously to a CFO, and it deserves to be stated precisely rather than waved at.

The fully loaded cost of onshore senior engineering talent has moved sharply. Think and Grow's 2025-26 Australian Tech Salary Guide, published in partnership with ACS Information Age, places senior software engineers at up to AUD 160,000 in base salary, with AI-focused and specialized roles considerably higher - Directors of AI averaging AUD 236,000. The ACS's own Digital Pulse 2025 report, based on a Deloitte-commissioned survey of nearly 800 technology workers, found that 77% believed they had insufficient skills in at least one digital capability required for their current role, with AI and cybersecurity the most prevalent gaps, directly inflating the wage premium for engineers who do hold these skills. Base salary, however, understates total cost to the company. After the Superannuation Guarantee's rise to 12% from 1 July 2025, payroll tax, recruitment overhead, benefits, and tooling, the fully-loaded cost of a single senior engineer in a major Australian metro frequently lands in the AUD 230,000–260,000 range. From 1 July 2026, Payday Super requirements, moving contributions from quarterly to per-pay-cycle remittance, add further payroll compliance overhead with no offshore equivalent.

Set against an embedded engineering model in a market like Vietnam, total compensation for an equivalent senior profile is materially lower. iTviec's Vietnam IT Salary and Recruitment Market Report 2025-2026, the most comprehensive local benchmark, drawing on tens of thousands of market data points, places senior back-end developers at approximately 54.9 million VND per month at high seniority. For engineers with international client exposure and FinTech or banking domain expertise, which is the relevant talent pool for an embedded banking engagement, VietnamDevs' 2026 guide to international recruitment benchmarks senior full-stack roles between USD 2,800 and USD 5,000 per month, translating to an annual total compensation range of approximately USD 34,000 to USD 60,000. Social insurance contributions in Vietnam are capped above a compensation threshold, meaning a higher-paid senior hire does not carry proportionally higher statutory overhead the way Australian superannuation does. Once both sides of the comparison are loaded for true total cost, not base salary against base salary, the realistic, audit-defensible saving on a like-for-like senior role lands between 40% and 65%.

That range matters because it's deliberately more conservative than the figures circulating in offshore marketing. An AUD 160,000 base salary compared against a USD 45,000 offshore salary looks like an 80%+ saving. Loaded for statutory cost, tooling, and management overhead on both sides, the defensible figure compresses, still substantial, but it's the number that survives a CFO's scrutiny and an internal audit's challenge, which is the number that actually matters.

Singapore changes the comparison, not the conclusion. SG developer rates have risen closer to Western benchmarks, which means the onshore-versus-insourced gap for an SG CTO is often wider in relative terms than for an AU counterpart, particularly given Singapore's even tighter senior-talent market and comparable AI-skill wage premiums.

But the more important shift is what the comparison should measure. Total Cost of Ownership for technology delivery extends well beyond salary arbitrage: recruitment, onboarding, domain training, attrition, vendor management overhead, rework, delivery delay, and knowledge loss at contract boundaries all belong in the calculation. Two delivery models can produce an identical TCO on day one and diverge sharply by year two, because one model loses institutional knowledge at every renewal and the other compounds against it. For strategic, continuously-evolving platforms: digital lending, AI-assisted decisioning, fraud detection, the more useful CFO question isn't "which model is cheaper this quarter," it's "which model produces a better return on technology spend across the life of the product." Those are frequently different answers and conflating them is the most common error in sourcing business cases that don't survive their first renewal negotiation.

Compliance Control in APAC Banking: Who Owns the Risk?

This is the section most cost-led comparisons skip and the one that actually decides the insourcing-versus-outsourcing question for a regulated institution.

Under CPS 230, accountability never transfers. The standard is explicit that an APRA-regulated entity's board and senior management remain responsible for operational resilience regardless of how a function is delivered. A bank can delegate execution; it cannot delegate the regulatory consequence. The standard requires a documented register of material service providers, contractual rights to audit and obtain information, and a tested plan for what happens if a provider fails, including the fourth-party providers a bank's own vendor depends on.

MAS's posture is structurally identical. Notices 658 and 1121 already require banks to assess, manage, and monitor risk arising from each outsourced relevant service, and the institution, not the vendor, carries that obligation. The forthcoming TPRM Guidelines widen this further, to third-party reliance generally rather than formal outsourcing alone.

The practical consequence: the compliance burden of outsourcing doesn't disappear under these frameworks; it becomes harder to discharge, because the bank is now accountable for governance over a relationship it doesn't operationally control. Every layer of subcontracting between the institution and the engineer's writing code against its core banking system is a layer that has to be documented, monitored, and explained to a regulator inside a 72-hour incident notification window.

This is also where AI governance and prudential compliance converge. A model in production needs the same continuous oversight as a critical operation: monitoring, retraining cadence, explainability evidence, and a clear chain of accountability for every change. When the engineers maintaining that model sit inside a multi-layered outsourcing structure, evidencing that oversight to a risk committee, let alone a regulator, becomes a documentation exercise built on assumptions about a vendor's internal practices the bank can't fully see.

Embedded insourcing collapses that chain. Engineers operate inside the bank's own access controls, change management processes, code repositories, and incident response runbooks. Security reviews, architecture boards, sprint planning, and model governance checkpoints become shared, real-time activities rather than externally reported ones. There's no fourth party register entry for "the subcontractor our vendor uses for overflow capacity," because there is no subcontractor, there's a delivery partner managing employment and operations for engineers who function, from a control's perspective, as an extension of the bank's own team. That doesn't remove the bank's CPS 230 or MAS TPRM obligations regarding the delivery partner itself - a documented arrangement, contractual audit rights, and a wind-down plan are still required, but it removes an entire layer of the third-party risk graph that traditional outsourcing introduces by design. The result isn't only stronger compliance. It's faster compliance: risk teams engage earlier; issues get resolved collaboratively inside the sprint rather than negotiated contractually after the fact.

Embedded insourcing collapses that chain. Engineers operate inside the bank's own access controls, change management processes, code repositories, and incident response runbooks. Security reviews, architecture boards, sprint planning, and model governance checkpoints become shared, real-time activities rather than externally reported ones. There's no fourth party register entry for "the subcontractor our vendor uses for overflow capacity," because there is no subcontractor, there's a delivery partner managing employment and operations for engineers who function, from a control's perspective, as an extension of the bank's own team. That doesn't remove the bank's CPS 230 or MAS TPRM obligations regarding the delivery partner itself - a documented arrangement, contractual audit rights, and a wind-down plan are still required, but it removes an entire layer of the third-party risk graph that traditional outsourcing introduces by design. The result isn't only stronger compliance. It's faster compliance: risk teams engage earlier; issues get resolved collaboratively inside the sprint rather than negotiated contractually after the fact.

Case Study: How an AU Mid-Market Bank Could Apply Embedded Insourcing

To make this concrete, consider a composite scenario representative of patterns seen repeatedly across AU mid-market ADIs and licensed payments providers moving through CPS 230 implementation in 2025-2026. This is an illustrative scenario built from common industry patterns, not a named client engagement.

A mid-market authorized deposit-taking institution is running a multi-year digital lending transformation, modernizing customer onboarding, introducing AI-assisted credit decisioning, and improving loan origination efficiency. Internal engineering capability was strong but constrained: several strategic initiatives were competing for the same scarce technology resources, and recruitment in Australia's tight digital-talent market wasn't keeping pace with the roadmap.

The bank had previously run this work through a traditional Australian systems integrator under a time-and-materials outsourcing arrangement. Two pressures converged in 2025: the integrator's day rates rose faster than the technology budget, and the bank's CPS 230 material service provider register exercise surfaced two offshore subcontracting layers behind the integrator that had never been formally assessed.

The bank restructured delivery around an embedded model instead. A core group of senior engineers, employed and operationally managed by an insourcing partner, joined the bank's existing product organization directly, working inside the bank's own Jira, Git, and CI/CD pipeline, governed by the bank's own change advisory board, and sitting alongside its internal architects, risk specialists, and product owners. Architectural decisions, code ownership, and production access stayed entirely with the bank's Sydney-based engineering leadership.

The outcomes that consistently show up in this pattern: a fully-loaded cost reduction in the 45-55% range for equivalent engineering capacity; a single, auditable material-service-provider register entry instead of a multi-layered subcontractor chain; and, counterintuitively for what started as a cost initiative, faster delivery velocity, because engineers embedded in the bank's own sprint cadence stopped losing time to outsourcing-style scope negotiation and change-order friction. Domain knowledge accumulated rather than reset with every renewal, and each release left the bank with more internal engineering maturity than the one before it.

Insourcing vs Outsourcing Decision Framework for Banking CDOs and CTOs

5 Questions to Ask Before Choosing an IT Delivery Model

Sourcing decisions are easiest to get wrong when they're framed as procurement rather than operating model design. Before defaulting to either traditional outsourcing or embedded insourcing, work through five questions:

- Is the initiative strategic or transactional? If the software directly shapes customer experience, competitive differentiation, or proprietary IP, long-term capability ownership matters more than short-term delivery price.

- Will regulatory oversight increase across the product's lifecycle? Anything touching AI, lending, payments, identity verification, or customer data typically demands sustained governance, not project-based delivery.

- Does institutional knowledge create durable advantages here? If engineers need deep, accumulated understanding of internal processes and regulatory obligations, retaining that knowledge inside the bank is itself a strategic asset.

- Will this platform keep evolving after launch? Continuous-delivery products favor stable engineering environments over rotating project teams that reset context at every handover.

- Is delivery speed constrained by funding or by recruitment? Across Australia and Singapore, technology hiring is the binding constraint far more often than budget. Embedded insourcing scales capacity without a 12-14-week domestic hiring cycle.

How to Evaluate an Insourcing Partner: A Due-Diligence Checklist

Not every provider marketing an "embedded team" delivers a genuine insourcing outcome, some simply relabel staff augmentation, and others deliver a standard dedicated team model without the compliance integration that regulated banking requires. The distinction matters: a dedicated team model gives you a stable pod of engineers aligned to your product over time, which is already a material improvement over rotating contractor. But in a CPS 230 or MAS-regulated environment, a "stable pod" is not sufficient; the team must operate inside your own control environment, not alongside it. Once the decision framework above points toward insourcing, use this checklist before signing:

- **IP and code ownership at the commit level. **The contract should assign all work products to your entity as it's created, not at project close-out. Confirm the partner's home jurisdiction has enforceable, internationally aligned IP law (Vietnam's amended IP Law, for instance, is TRIPS-compliant via WTO membership, verify the equivalent for any market under consideration).

- **Security posture you can actually audit. **ISO 27001 certification, SOC 2 reporting, and a contractual willingness to submit to your own internal audit and penetration testing schedule, not just the partner's own attestations.

- Governance that maps to CPS 230 / MAS TPRM, not around it. Ask directly: can this partner sit inside your material service provider register as a single, transparent entry? Will they support your 72-hour incident notification obligations with real-time visibility rather than a quarterly report?

- **Talent retention data, not headcount claims. **Senior engineer attrition is the single biggest hidden risk in any offshore or insourced model. Ask for retention rates by seniority band, not total engineer counts.

- **Timezone overlaps that support real-time collaboration. **A 2-4 hour offset, as with Vietnam against AEST or Singapore time, supports daily stand-ups and live pairing; a 10+ hour offset structurally doesn't, regardless of the sales deck.

- A documented, time-bound exit plan. CPS 230 explicitly expects contingency and exit arrangements for material service providers. A credible insourcing partner proposes a 60–90-day wind-down with full handover documentation as a standard contract term, not a negotiated concession.

- Pricing transparency at the FTE level. Insourcing should price like a transparent extension of payroll, an all-in monthly cost per engineer, not a project SOW with margin layered at multiple points in a subcontracting chain.

The sourceCode Embedded Team Model for APAC Banks

sourceCode exists because regulated APAC financial institutions need a delivery model built around CPS 230 and MAS's third-party risk regime from day one, not a generic offshore staffing arrangement retrofitted onto a banking client after the fact.

In practice, that means engineering talent that operates as a genuine extension of your own team: embedded in your sprints, governed by your security controls, accountable to your engineering leadership, and present in your product planning rather than waiting on a statement of work. It means talent sourced from a market with a structurally lower and more predictable cost base than AU or SG onshore hiring, in a timezone that supports real-time collaboration rather than asynchronous handoff. It means a single, transparent entity in your risk and compliance function can register, assess, and audit, rather than a chain of subcontractors discovered during your next material service provider review. And it means architecture, IP, and institutional knowledge that compounds with your bank for the life of the relationship and stay there after it.

This is, deliberately, neither traditional outsourcing nor wholesale internal hiring. It's an engineering partnership built for institutions where technology capability, governance, and long-term knowledge retention matter as much as delivery speed, which, in AI-driven banking under CPS 230 and MAS's tightening scrutiny, is now most of the work that matters.

Conclusion

The sourcing debate in banking technology has moved past "build versus buy." The more useful question for 2026 is whether the work in front of you is project-shaped or capability-shaped, and increasingly, in a market defined by production AI, continuous delivery, and prudential regulators who have made clear that accountability never transfers, most of the work that matters to a CDO or CTO's roadmap is capability-shaped.

Where the answer to that question is yes, insourcing, not outsourcing, is the model built for the regulatory and competitive environment you're actually operating in. Cost still matters, and the 40-65% TCO saving on a fully-loaded basis is real and defensible. But it's no longer the only KPI. Engineering continuity, regulatory alignment, institutional knowledge, and the rate at which capability compounds across releases have become equally decisive and they're the factors that determine whether a sourcing decision still looks right at the next contract renewal, not just at signing.

Key Takeaways

- The economics of IT sourcing have shifted from labor arbitrage to total capability ownership; Total Cost of Ownership is a more meaningful metric than day rates alone.

- CPS 230 (effective 1 July 2025) and MAS's Notices 658/1121 plus its proposed TPRM Guidelines confirm that accountability for critical operations and third-party risk cannot be outsourced, only execution can.

- AI-enabled banking platforms require continuous engineering ownership: monitoring, retraining, governance, not project-based delivery that ends at implementation.

- A fully-loaded cost comparison (not salary-to-rate) puts realistic AU-onshore-to-APAC-insourced savings at 40-65%, with Vietnam's capped social insurance structure adding further predictability above SG/AU equivalents.

- Embedded insourcing combines external delivery capacity with internal governance, collapsing with the fourth-party risk chain that traditional outsourcing introduces by design.

- The decision isn't outsourcing versus insourcing in the abstract, it's matching the operating model to whether the work in front of you is transactional or strategic.

About sourceCode

sourceCode partners with banks, insurers, and licensed financial institutions across APAC to build long-term engineering capability through embedded delivery teams. By combining senior software engineering expertise with operating familiarity in regulated industries, we help institutions accelerate AI and digital transformation while keeping governance, compliance, and architectural control where it belongs, inside the bank.

Explore how embedded insourcing can help your organization scale delivery without giving up control. Talk to our Banking Technology Specialists

This article reflects publicly available regulatory guidance from APRA and MAS current as of mid-2026, and market salary and cost benchmarks drawn from published Australian and Vietnamese labour market data. Regulatory requirements evolve, confirm current CPS 230 and MAS TPRM obligations directly with APRA, MAS, or qualified legal counsel before making compliance-dependent decisions.