IT Outsourcing for APAC Banks: When It Still Makes Sense

For more than a decade, the banking industry has framed technology sourcing as a binary choice.

Outsource to reduce costs and access specialist capacity. Or build internally to retain control and institutional knowledge. That framing has become too simple for the environment APAC banking leaders are actually operating in. The question facing an Australian CDO or Singapore CTO in 2026 is no longer "Should we outsource?" It's a more precise question:

Which technology workstreams create strategic advantages, and which should simply be delivered efficiently?

That distinction matters because the most expensive sourcing mistakes aren't made by choosing outsourcing or insourcing as a philosophy. They're made by applying the wrong model to the wrong category of work. A bank that outsources its core AI decisioning platform is creating vendor dependency on a capability it will need to govern for life. A bank that builds a permanent internal team around routine infrastructure monitoring is spending scarce engineering talent on work that doesn't compound in value.

The most effective financial institutions in APAC are moving away from organization-wide sourcing positions and toward a portfolio-based sourcing strategy, one that evaluates each technology domain independently, based on its strategic value, rate of change, regulatory exposure, and the importance of long-term institutional knowledge.

This article is the companion to our IT Insourcing vs. Outsourcing for APAC Banks: A Strategic Decision Framework for 2026, which makes the case for why embedded insourcing outperforms traditional outsourcing for regulated, AI-driven, continuously evolving banking platforms. That case stands. But it would be intellectually dishonest and commercially convenient to stop there.

There are categories of technology work where outsourcing, structured and governed correctly, remains not just acceptable but genuinely superior to insourcing. This article maps exactly where those categories are, where the line falls, and what distinguishes a sourcing decision that holds up from one that doesn't.

Outsourcing vs Insourcing in APAC Banking: Output Delivery vs Capability Building

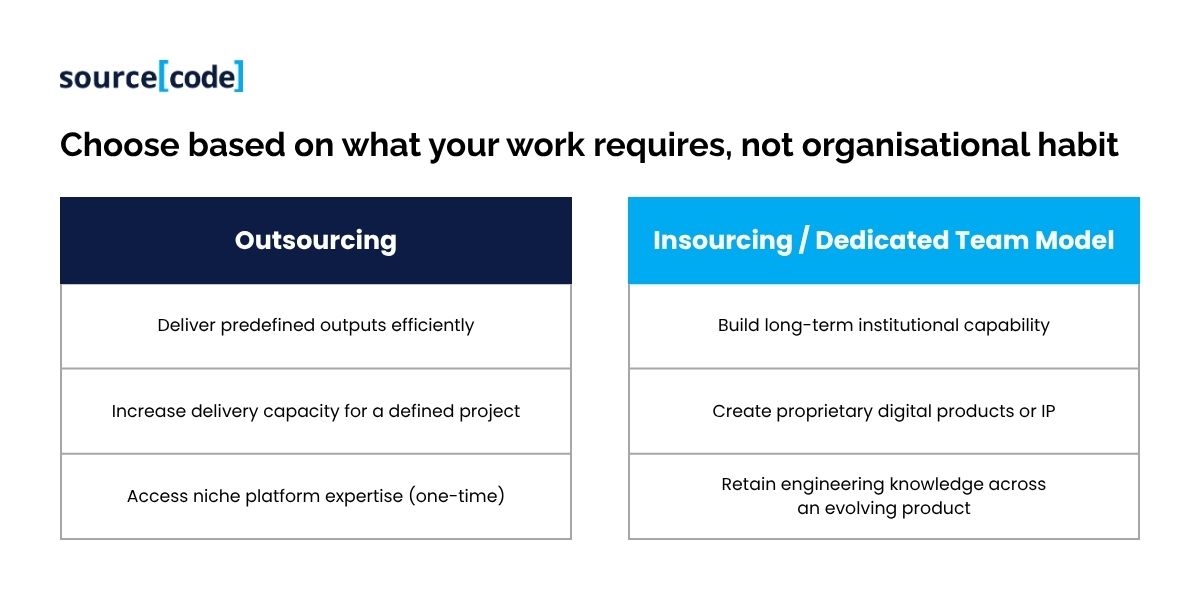

The most common sourcing error isn't choosing the wrong vendor. It's applying a delivery-optimized model to a capability problem, or a capability-building model to a delivery problem.

Outsourcing and insourcing are not competing philosophies. They optimize for different outcomes.

Viewed through this lens, the sourcing decision becomes significantly cleaner.

Work that is predictable, repeatable, and operationally stable typically benefits from external delivery. Work that continuously evolves alongside customers, regulation, and business strategy generally requires stronger internal ownership.

This distinction is particularly important in banking because technology is no longer merely supporting business operations; it increasingly defines competitive advantage. Digital onboarding journeys, AI-driven lending decisions, fraud detection models, and embedded finance capabilities cannot be treated as traditional IT projects. Infrastructure monitoring and legacy batch-processing maintenance often can.

As Forrester observed in its Predictions 2026: Asia Pacific report (October 2025), decades of outsourcing across the region have created what Forrester describes as "vendor coordination muscle memory", a structural inertia that slows agile adoption and creates genuine barriers to building internal product capability. Understanding which work genuinely belongs in outsourcing, and which only feels familiar there because of that accumulated habit, is the practical discipline this framework is designed to support.

When to Outsource IT Infrastructure and Managed Services in APAC Banking

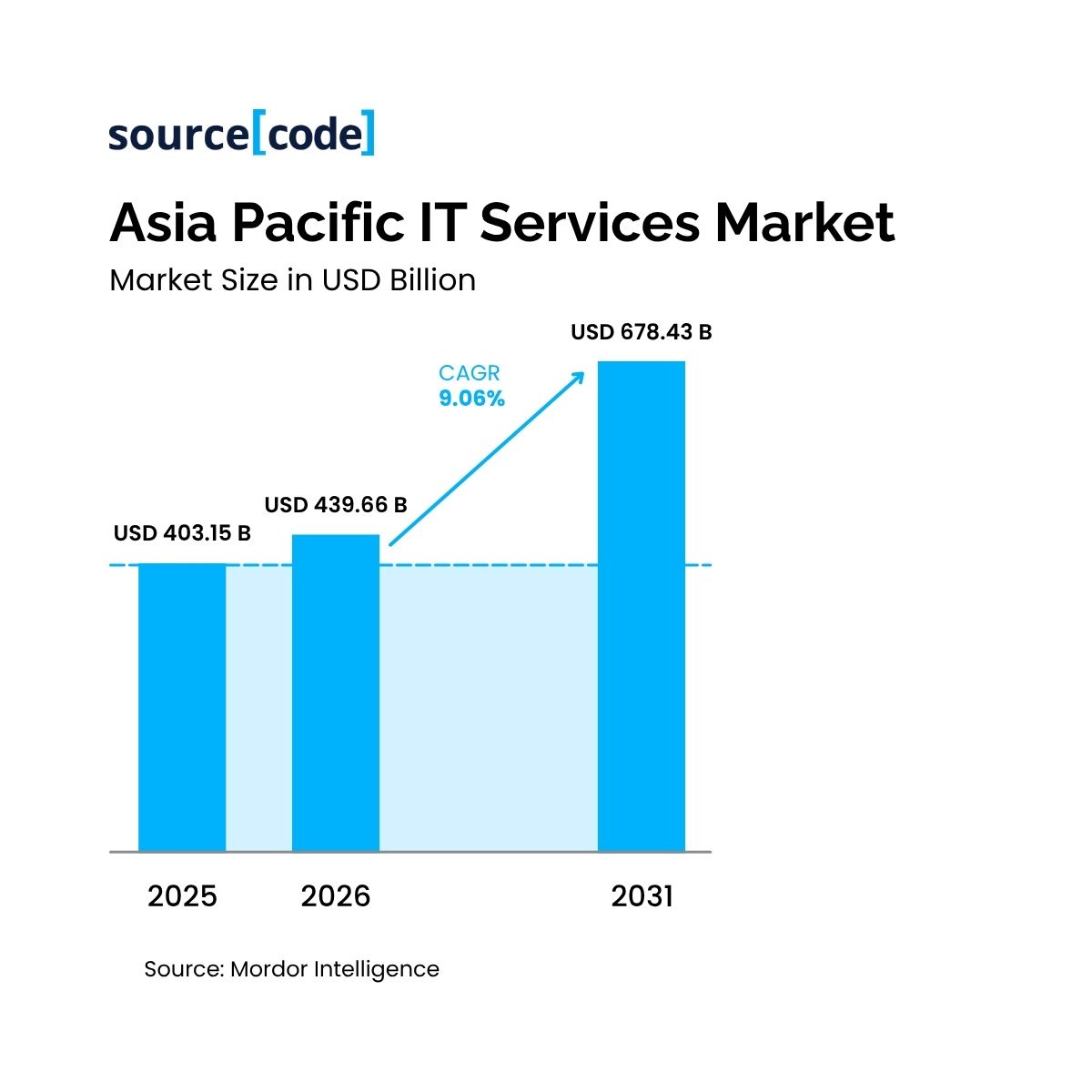

Among all banking technology domains, infrastructure operations remain one of the strongest candidates for outsourcing, and the market data reflects how consistently well the model has worked here.

Source: Mordor Intelligence (June 2026)

Source: Mordor Intelligence (June 2026)

Mordor Intelligence's February 2026 APAC IT Services market analysis values the regional IT services market at USD 439.66 billion in 2026, projected to reach USD 678.43 billion by 2031, with IT infrastructure outsourcing retaining a 32.74% share of the market as of 2025. Banking, financial services, and insurance represent the single largest end-user sector, accounting for 24.62% of APAC IT services spending in 2025. Infrastructure managed services remain the largest component of that spending, not because banks haven't tried to bring infrastructure in-house, but because the outsourcing model genuinely fits the operational characteristics of infrastructure work.

The reasons are structural. Infrastructure operations are highly standardized: SLAs for uptime, patch cadence, incident response times, and change management procedures are well-understood and measurable. A managed services provider can be held accountable to precise, quantifiable commitments in ways that application development vendors cannot. Infrastructure is also inherently round-the-clock. An AU bank paying Sydney onshore rates for overnight network operations support is paying a structural premium for work a follow-the-sun managed services provider can deliver more efficiently without any loss of control.

Critically, outsourcing infrastructure does not mean relinquishing governance. Leading institutions retain ownership of architecture decisions, security standards, vendor management, compliance oversight, and technology strategy. Execution is outsourced. Accountability remains internal. This governance model aligns directly with APRA CPS 230 expectations around material service providers and MAS outsourcing guidance, both of which place responsibility with the regulated institution regardless of how delivery is structured.

Best suited for outsourcing:

- Cloud infrastructure operations and monitoring

- Service desk and endpoint management

- Network operations (NOC)

- Backup and disaster recovery

- Routine security operations under defined governance frameworks

- Workplace IT support

Where this breaks down: When "infrastructure" begins to blur into "platform engineering." A bank that outsources cloud infrastructure to one vendor and application hosting to another, then attempts to build a cloud-native data platform on top, will find that the gaps between managed service boundaries become delivery bottlenecks. The cleaner the separation between managed infrastructure and internal product engineering, the better outsourcing works.

Outsourcing Legacy System Maintenance for APAC Banks: When It Works

Almost every mid-market bank in Australia and Singapore carries legacy technology debt, core banking systems on decades-old COBOL or Java stacks, loan origination platforms that pre-date mobile banking, payment processing infrastructure that has been patched and extended but never modernized.

Maintaining these systems is a genuine, important work. It keeps the bank running. But it is emphatically not strategic. No competitive advantage is created by fixing a bug in a 2003-era batch processing job. The engineers who maintain these systems need deep knowledge of specific, often obscure technology stacks, but the work itself is stable, bounded, and unlikely to change fundamentally.

This is outsourcing territory, and a useful diagnostic question for technology leaders is:

“Does maintaining this platform create future competitive advantage, or merely preserve today's operations?”

If the answer is the latter, outsourcing often represents the more efficient allocation of scarce senior engineering talent.

Specialist legacy maintenance providers, particularly those with deep COBOL, Java EE, or early-generation core banking expertise, can carry this work at significantly lower cost than an insourced team. The institutional knowledge required is knowledge of a static system, not of an evolving product, and that distinction removes the capability-compounding argument for insourcing that applies to digital products.

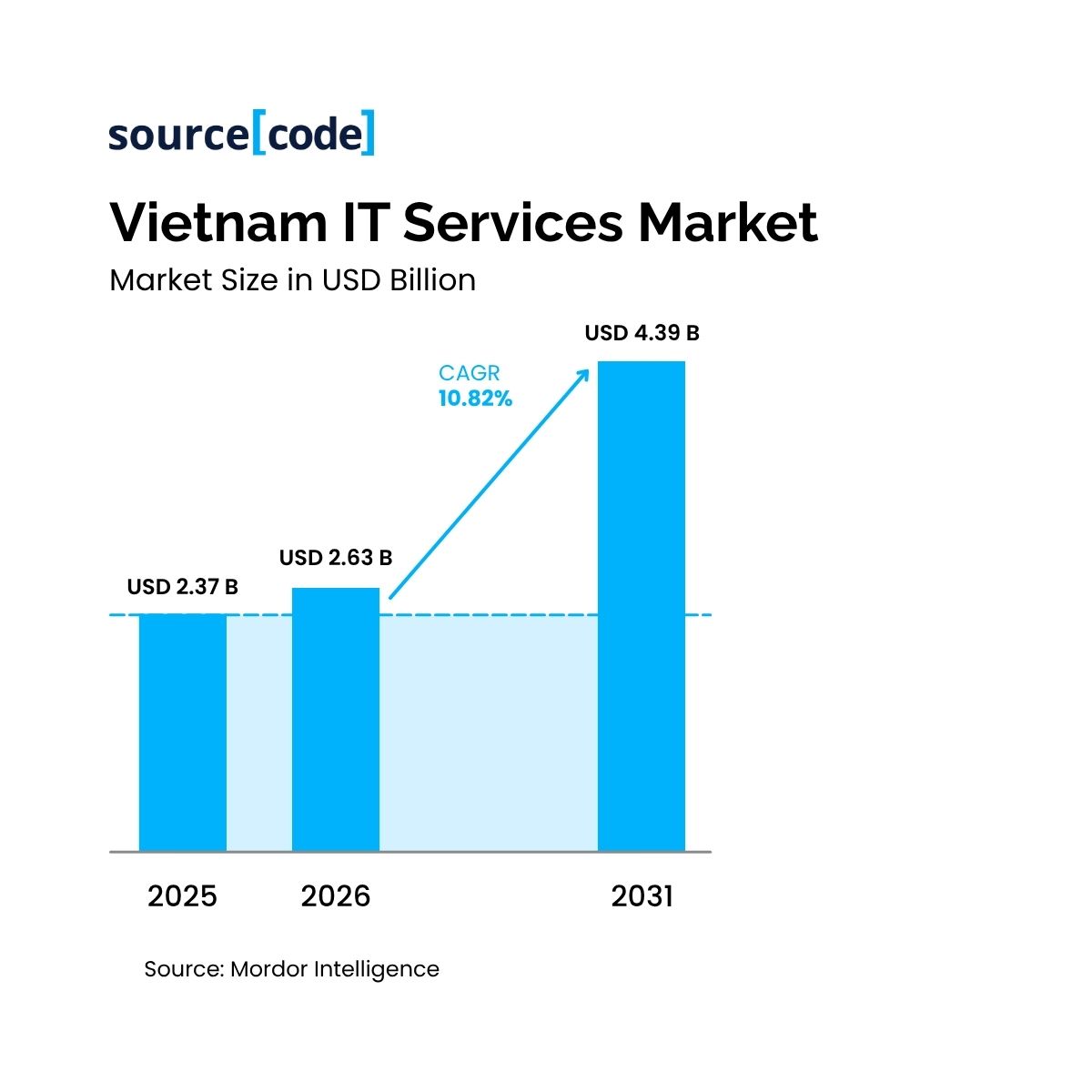

Vietnam has become one of the primary APAC markets for legacy banking system specialists. Mordor Intelligence places Vietnam's IT services market at USD 2.37 billion in 2025, forecast to reach nearly USD 4 billion by 2030.

Outsourcing legacy maintenance succeeds, however, only when knowledge transfer is structured explicitly. Banks should avoid creating vendor dependencies where critical system knowledge gradually migrates entirely outside the organization. Successful operating models include detailed documentation of ownership, shared architecture repositories, internal technical governance, regular knowledge reviews, and clearly defined transition plans. Legacy maintenance should reduce operational burden, not reduce institutional knowledge.

Best suited for outsourcing:

- COBOL, Java EE, or early-generation core banking support

- Defect remediation and incident response on stable systems

- Regulatory update implementation on legacy platforms

- Operational continuity management for non-strategic systems

Where this breaks down: When "maintenance" quietly expands to include integrations with new systems, or when the legacy system needs to behave like a modern API-driven platform. At that point, the static-knowledge advantage of a legacy specialist becomes a static-knowledge liability.

When Should APAC Banks Outsource App Development? Fixed-Scope Projects That Fit

Not every software project deserves a permanent engineering team or an embedded delivery model. Across banking technology portfolios, many initiatives are well-defined, low-risk, and unlikely to evolve into strategic digital products: internal workflow applications, reporting portals, administrative tools, regulatory forms, document management systems, and compliance-driven integrations with predictable scope.

For these projects, the business objective is simple: deliver agreed functionality on time, within budget. External delivery partners typically bring established development processes, reusable components, and flexible team structures that allow banks to scale capacity without adding permanent headcount. Procurement is cleaner, delivery milestones are easier to define, and commercial outcomes are more predictable.

This use case comes with an important caveat, and it's the one most frequently ignored: the sourcing error that turns a commodity project into an outsourcing failure is mislabeling strategic, evolving work as "fixed scope" for procurement convenience or to reduce short-term costs.

Before outsourcing any application development, leadership teams should apply three honest diagnostic questions:

1. Will this product require continuous iteration based on customer behavior or business strategy over the next 12–24 months?

2. Does this application create meaningful competitive differentiation for the bank?

3. Will regulatory oversight of this product increase across its lifecycle?

If the answer is yes to any of these, the project is unlikely to remain fixed-scope, and applying an outsourcing contract to it will produce change-order friction, vendor dependency, and knowledge loss at precisely the point when the bank most needs engineering continuity.

Best suited for outsourcing:

- Internal business applications with stable requirements

- Regulatory reporting portals with defined scope

- Employee self-service and workflow automation tools

- Document management systems

- Well-defined API integrations with limited future enhancement scope

- Short-term digital campaigns with a fixed end date

Core Banking and Payment Implementations in APAC: Where Specialist Outsourcing Fits

Some banking programs demand expertise that few institutions can justify maintaining permanently. Core banking modernization, payment infrastructure upgrades, and major platform implementations fall into this category; work that requires deep, vendor-specific technical knowledge that may only be needed once per decade.

Examples include:

- Implementing a new core banking platform such as Temenos Transact or Thought Machine Vault Core

- Integrating domestic real-time payment schemes such as Australia's New Payments Platform (NPP) or Singapore's PayNow

- Large-scale cloud migration programs

- Enterprise data platform implementation under APRA or MAS data governance frameworks

- Identity and access management transformation

For these programs, the model that works is not wholesale outsourcing; it's a hybrid. Internal architecture teams and program governance retain ownership of technology direction, security standards, and business outcomes. Specialist implementation partners bring certified platform expertise, proven delivery methodologies, and a deep bench of consultants with specific scheme or vendor knowledge. The objective is to accelerate execution and reduce implementation risk, not to outsource strategic ownership.

Once implementation is complete, responsibility for product evolution, operational governance, and business capability should progressively transition back to internal teams. The knowledge transfer plan isn't an afterthought; it's a contractual deliverable.

CPS 230 note: Large one-time implementations frequently qualify as material service provider arrangements for their duration, particularly when the implementation covers a critical operation. The critical discipline is ensuring your CPS 230 register reflects the engagement for its full duration — not just post-go-live — and that exit and contingency provisions cover mid-implementation failure scenarios, not only delivery completion.

Where Does IT Outsourcing Fail in APAC Banking? 3 Consistent Patterns

If outsourcing continues to create genuine value across infrastructure, legacy maintenance, commodity development, and specialist implementation, why do so many banking outsourcing programs underperform?

The failure pattern is remarkably consistent. It rarely comes from geography, labor cost, or vendor quality. It comes from assigning strategic capabilities to delivery models designed for operational efficiency.

Pattern 1: Continuous digital products. Any digital product that will evolve regularly after launch, a mobile banking app, a digital onboarding journey, an AI-assisted credit decisioning tool, is not an output problem. It is a capability problem. Outsourcing it produces a vendor dependency that compounds with every release: each enhancement requires renewed context transfer, each sprint requires re-establishing shared understanding, and each renewal negotiation happens against a backdrop of accumulated knowledge the vendor holds and the bank doesn't. The APRA HESTA enforcement action of mid-2025, in which APRA imposed additional license conditions after a superannuation fund failed to adequately oversee a transition to an outsourced administration provider, leaving over a million members without access to funds for weeks — illustrated at enforcement level the consequences of insufficient oversight over outsourced functions. Digital products require the same sustained internal ownership that APRA now explicitly expects for critical operations.

Pattern 2: AI and machine learning in production. A trained model is not a delivered piece of software. It is the beginning of a permanent operational obligation: monitoring for drift, periodic retraining, bias assessment, explainability documentation, and governance sign-off for every material change. These responsibilities run for the life of the model in production. No outsourcing contract has a natural structure for this obligation, because outsourcing was designed for finite deliverables. Banks that fully outsource production AI capabilities risk losing visibility into how critical models evolve, making governance, regulatory compliance, and continuous improvement significantly harder to evidence. APRA's System Risk Outlook of November 2025 signaled that the regulator is now actively collecting data on material service provider concentrations and cross-institutional dependencies, a direction of travel that makes institutional visibility into AI systems progressively more important, not less.

Pattern 3: Regulated critical operations under CPS 230 and MAS oversight. The accountability principle under both CPS 230 and MAS's third-party risk framework is unambiguous: the regulated entity is responsible for outcomes regardless of delivery model. For operations where a regulator will question the bank's own understanding of what is happening and why, core risk systems, fraud detection, customer data governance, outsourcing creates a gap between accountability and operational visibility that is genuinely difficult to close, and increasingly difficult to defend to a supervisory authority. The fourth-party risk problem is most acute precisely where regulators are most likely to look: when the bank can see its vendor but cannot readily see who the vendor depends on.

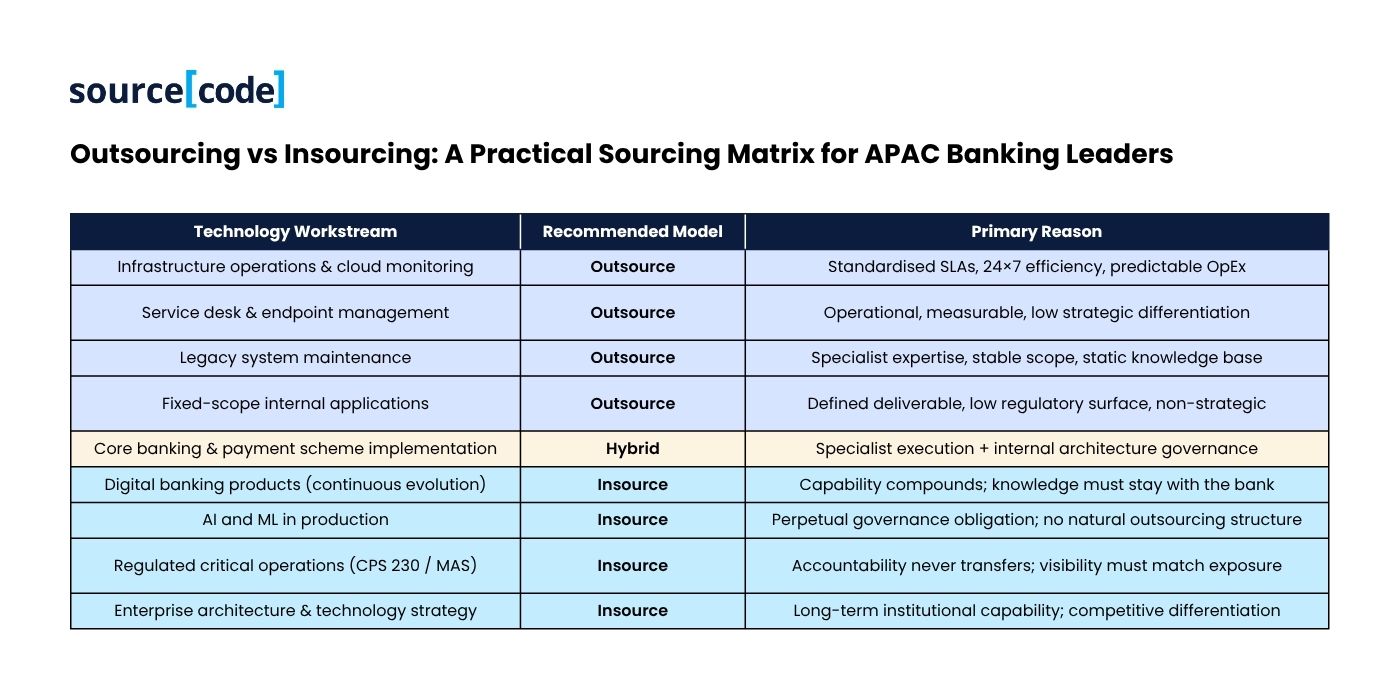

Outsourcing vs Insourcing: A Practical Sourcing Matrix for APAC Banking Leaders

Rather than choosing between outsourcing and insourcing at an organizational level, executive teams should evaluate each workstream independently. The matrix below maps common banking technology categories to the delivery model that best fits their operational characteristics.

The discipline required is honest categorization. Work that is actually continuous, strategic, or regulated should not be placed in the "outsource" column simply because it's easier to procure that way. That categorization error is where the outsourcing failure stories consistently begin, and where the regulator eventually arrives.

Choosing the Right IT Delivery Model: How sourceCode Approaches APAC Banking

Technology sourcing is not a procurement exercise. It is a capability strategy.

The strongest banking organizations in APAC are not those that outsource everything or insource everything. They are the ones that deliberately separate operational execution from strategic capability building, and work with partners who will tell them honestly which is which.

Infrastructure can be purchased. Engineering capability cannot. Specialist implementation expertise can be engaged when required. Institutional knowledge must be cultivated over time.

sourceCode delivers both outsourcing and insourcing models because APAC banks need both. For infrastructure managed services, legacy maintenance, and fixed-scope commodity development, a well-structured traditional outsourcing engagement is the right answer, and we will say so directly, even when an insourcing engagement would be more commercially convenient for us.

For regulated, AI-driven, continuously evolving banking platforms, the category where embedded insourcing was built, the data and regulatory framework that supports that conclusion is laid out in our companion article: [IT Insourcing vs Outsourcing for APAC Banks: A 2026 Decision Framework].

The goal is not to promote a single sourcing model. It is to help banking technology leaders match the right delivery structure to the right category of work, and to make that decision with clear eyes about what each model costs, controls, and produces over the life of a program.

Because competitive advantage in modern banking is not determined by where software is built. It is determined by which capabilities the organization chooses to own.

Key Takeaways

- Outsourcing is not a failed model - it's a frequently misapplied one. Failure is almost always a mismatch between delivery model and work type.

- The fundamental distinction: outsourcing optimizes for output delivery; insourcing optimizes for capability building. The right model depends entirely on what the work requires.

- Outsourcing consistently delivers value in infrastructure managed services, legacy system maintenance, fixed-scope commodity development, and specialist one-time implementations.

- Outsourcing consistently underperforms continuous digital products, AI/ML in production, and regulated critical operations under CPS 230 or MAS oversight, the categories where institutional knowledge is itself a strategic and regulatory asset.

- Applying three honest diagnostic questions before outsourcing any application development, will it evolve continuously? does it differentiate the bank? will regulatory oversight increase?, prevents the most common and costly sourcing error.

- A technology partner worth working with will recommend outsourcing where it genuinely creates value and advise against it when insourcing will produce better long-term outcomes. That distinction separates strategic advisors from delivery vendors.

Frequently Asked Questions

Is IT outsourcing still relevant for banks in 2026?

Yes. In specific categories. Outsourcing remains highly effective for infrastructure management, legacy system maintenance, fixed-scope application development, and specialist implementation projects such as core banking platform deployments. The model's relevance depends entirely on the type of work being outsourced, not on outsourcing as a principle. Strategic capabilities, digital products, AI platforms, regulated critical operations, are increasingly being managed internally by leading APAC banks.

What is the difference between outsourcing and insourcing in banking technology?

Outsourcing focuses on efficient delivery of defined outputs through external partners. Insourcing focuses on building long-term institutional capability and retaining critical engineering knowledge within the organization. The embedded insourcing model, specifically, combines external talent from lower-cost markets with full integration into the bank's own governance, sprint cadence, and architecture ownership, keeping all strategic knowledge internal while achieving significant cost savings over onshore hiring.

Should APAC Banks Outsource AI Development?

Banks may engage external specialists during initial AI model development or platform selection. However, production of AI capabilities, including model monitoring, drift detection, retraining cycles, bias assessment, and governance documentation, are significantly stronger when owned internally. APRA's CPS 230 and MAS's third-party risk framework both require regulated entities to maintain clear accountability over operations, and AI systems in production are operational systems in the most demanding regulatory sense.

How should APAC banks decide between outsourcing and insourcing?

Evaluate each technology workstream across four dimensions: strategic value (does this differentiate the bank?), rate of change (will requirements evolve continuously?), regulatory criticality (does CPS 230 or MAS guidance apply?), and institutional knowledge value (does deep organizational knowledge compound here?). Capabilities that score high across these dimensions are typically stronger candidates for insourcing. Stable, operational workloads with low strategic differentiation are generally strong candidates for outsourcing.

What Is the Embedded Insourcing Model for APAC Banking?

Embedded insourcing is a delivery model where engineers are sourced from a market with a more favorable cost and talent structure, typically Vietnam for APAC banking clients but operate entirely inside the bank's own governance, sprint cadence, tooling, and product organization. Unlike traditional outsourcing, embedded insourcing keeps architecture decisions, IP ownership, and institutional knowledge with the bank. Unlike direct domestic hiring, it achieves a fully loaded TCO saving of 40-65% compared to Australian or Singapore onshore equivalents, without the 12–14-week average hiring cycle for senior domestic roles.

Not sure which model fits your current technology program?

Most sourcing decisions aren't as clear-cut as the matrix above suggests. Portfolios contain mixed workstreams. Programs start as one category and evolve into another. Regulatory requirements shift mid-delivery.

If you're working through a sourcing decision for a specific program, whether it should stay in outsourcing, move to insourced delivery, or sit in a hybrid model, our Banking Technology Specialists can work through the framework with you in a single session.

→ [Talk to a Banking Technology Specialist, no sales pitch, just the framework applied to your specific situation.]

About sourceCode

sourceCode partners with banks, insurers, and licensed financial institutions across APAC to build long-term engineering capability through embedded delivery teams, and to structure outsourcing engagements correctly where that model genuinely fits. By combining deep software engineering expertise with operating experience in regulated industries, we help institutions match the right delivery model to the right work and execute both with the governance rigor that CPS 230 and MAS requirements demand.

This article reflects publicly available regulatory guidance from APAC and MAS current as of mid-2026, and third-party research from Forrester, Mordor Intelligence, and the Australian Computer Society. Regulatory requirements evolve, confirm current CPS 230 and MAS TPRM obligations with APRA, MAS, or qualified legal counsel before making compliance-dependent decisions.

Sources

- Predictions 2026: APAC Leaders Choose Pragmatism Over Hype In The Age Of AI”, Forrester, (October 28, 2025)

- Asia Pacific IT Services Market Size & Share Analysis - Growth Trends And Forecast (2026 – 2031), Mordor Intelligence, (June 18, 2026)