Agentic AI in APAC Banking: From Pilot to Production - A 2026 Blueprint for CIOs, CDOs and Heads of Digital

Agentic AI has become the fastest-growing category of enterprise technology in 2026. Gartner (2026) projects agentic AI software spending to reach US$206.5 billion this year, a 139% increase over 2025, and forecasts that 40% of enterprise applications will embed task-specific agents by year-end. Yet Deloitte's 2026 Tech Trends survey found that only 11% of organizations have agentic AI actually running in production, while 35% have no strategy at all.

In Asia-Pacific banking, the same asymmetry is visible. Nearly 80% of financial institutions in Asia report using AI in some form (McKinsey, 2026), and Singapore's DBS Bank has scaled to more than 370 use cases powered by 1,500-plus models, contributing an incremental S$1 billion in 2025 revenue (CNBC, 2025). At the same time, on 30 April 2026 the Australian Prudential Regulation Authority (APRA) issued an industry-wide letter warning that AI governance is "not keeping pace" with adoption, calling out agentic and autonomous workflows as a specific supervisory concern (APRA, 2026).

This article sets out a five-part blueprint for moving from agentic AI pilots to enterprise-grade production in banking, insurance and financial services across APAC. It draws on regulatory guidance from MAS, HKMA and APRA; adoption data from McKinsey, BCG, Deloitte and Gartner; and operational learnings from leading APAC banks. The central argument: the winners in 2026-2028 will not be the banks that build the most agents, but those that industrialize agent lifecycle management: governance, identity, observability, and human-in-the-loop controls as a first-class engineering discipline.

Why 2026 Is the Inflection Point

Banking has moved through three distinct waves of AI adoption. Predictive AI powered credit scoring, fraud detection, and churn models for more than a decade. Generative AI, deployed at scale from 2023 onwards, unlocked copilots for relationship managers, code generation for engineering teams, and document automation across trade finance and compliance. Agentic AI is the third wave, systems that plan, act, and coordinate across multiple tools and workflows with progressively less human intervention.

BCG (2026) describes the current moment as banking's "AI reckoning": early experimentation is behind us, and boards are asking why AI-related spending, which now consumes 15-20% of technology budgets in APAC's tier-one banks, has produced only marginal improvements to cost-to-income ratios. The MIT-linked NANDA study cited in industry press found that 95% of enterprise generative AI pilots have delivered no measurable P&L impact, a data point that has forced a hard conversation between CIOs and CFOs.

Agentic AI is being positioned as the answer. McKinsey (2026) argues that agents can compress banking operations cost structures by 20-30% by 2028, chiefly by collapsing the handoffs between systems that today consume the majority of front-, middle- and back-office effort. In Asia specifically, the productivity dividend is amplified by three structural factors: high wage-inflation in operations centers (Manila, Kuala Lumpur, Ho Chi Minh City); a young, mobile-first customer base demanding real-time service; and rapid regional regulatory harmonization around real-time payments and open finance.

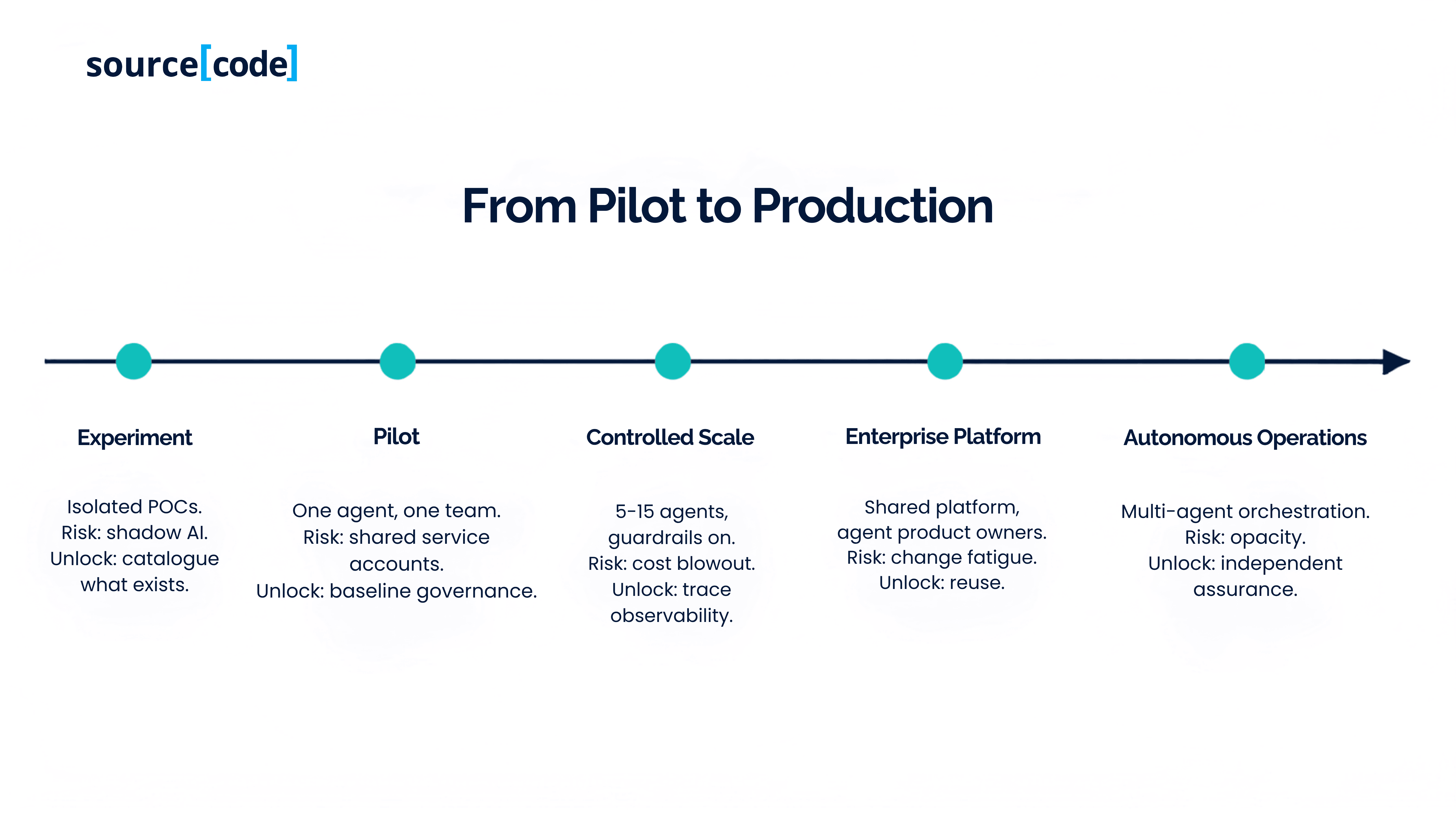

Why 89% of Banks Are Still Stuck in Pilot

The gap between adoption and production has four root causes.

Data readiness remains the primary constraint. Agents that plan and act cannot tolerate the fragmented customer, product, and reference data that most banks live with. In interviews with 50 APAC bank technology leaders, Capco (2025) identified data lineage, entitlement and quality as the single most cited blocker to agentic scale-up, well ahead of model performance.

Non-human identity is a supervisory blind spot. APRA (2026) explicitly flagged that "identity and access management capabilities have not yet adjusted to non-human actors such as AI agents." The vast majority of banks still assign agents shared service accounts, which breaks the principle of least privilege, prevents attribution, and creates uninsurable operational risk. Until IAM, PAM and IGA platforms treat agents as first-class identities with just-in-time entitlements, agents cannot safely operate in production.

Investment is skewed toward technology, not the operating model. Deloitte (2026) found that 93% of AI-related spending flows to infrastructure and licenses, and only 7% to talent, training, change management, and governance. This mirrors the mistake many banks made in the early cloud era: the platform arrives, but the organization does not adapt.

Return-on-investment discipline is immature. Gartner (2026) warns that more than 40% of agentic AI projects will be cancelled by 2027 because of rising unit economics and unclear value capture. Token costs have fallen 10x year-on-year, but agentic workflows, which involve multi-step reasoning, tool use and re-planning, can consume 50-200x for the tokens of a single-shot prompt. Without cost observability at the agent level, banks lose the ability to price internal services.

Key Trends Reshaping APAC BFSI in 2026

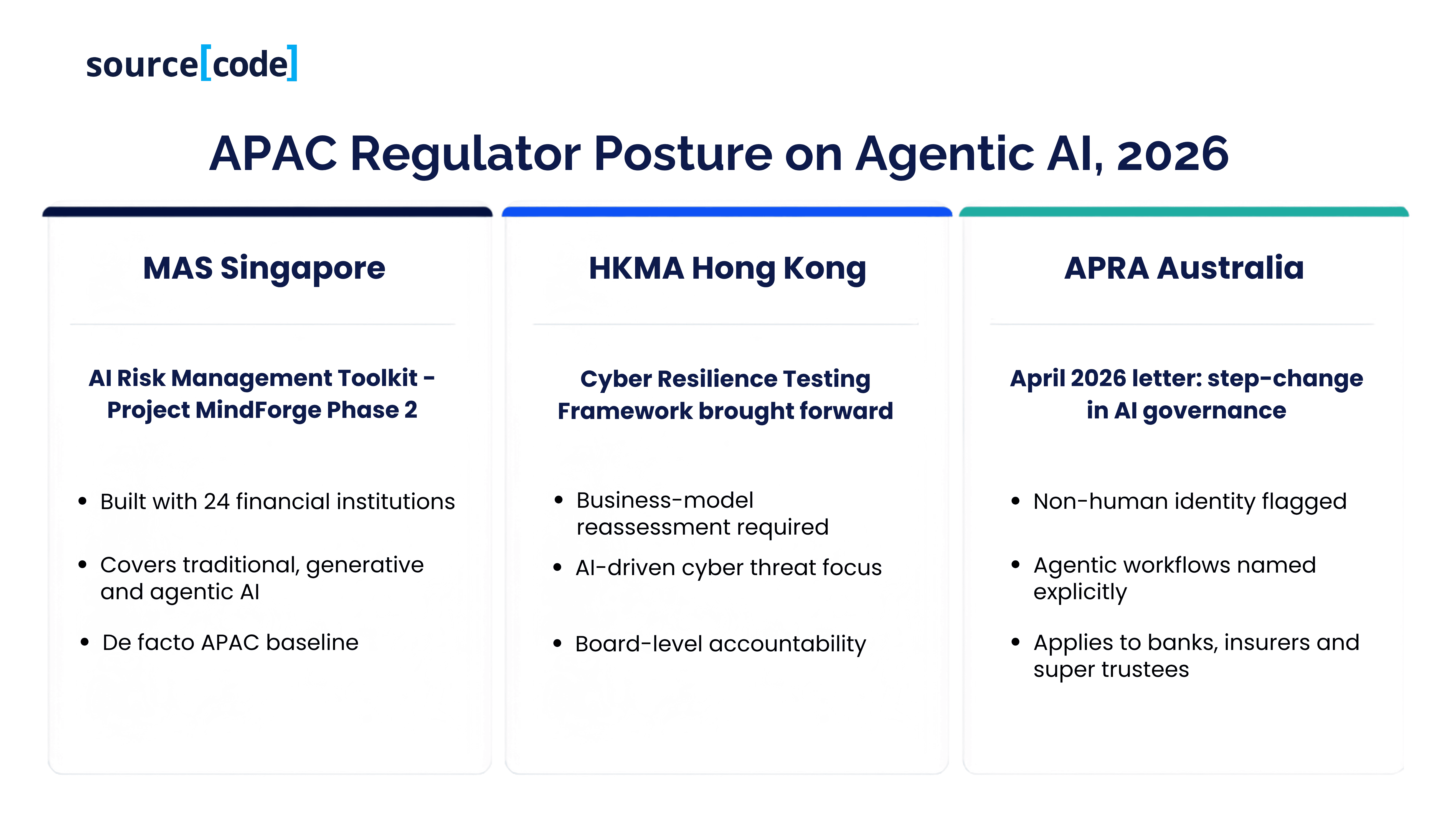

Trend 1: Regulators are moving from principles to prescriptions. The Monetary Authority of Singapore (MAS) closed Phase 2 of Project MindForge in early 2026 with the publication of an AI Risk Management Toolkit developed with 24 financial institutions (MAS, 2026). The toolkit distinguishes between traditional AI, generative AI and emerging agentic AI, and specifies control expectations for each. The Hong Kong Monetary Authority (HKMA) has brought forward a Cyber Resilience Testing Framework and required authorized institutions to reassess business models in light of AI-driven change (HKMA, 2026). APRA's April 2026 letter calls for a "step-change" in governance, risk management, assurance, and operational resilience for AI.

Trend 2: Agentic commerce is arriving faster than expected. In 2026, DBS became the first Asia-Pacific issuer to pilot Visa Intelligent Commerce, enabling AI agents to make everyday payments on behalf of customers (DBS, 2026). Mastercard executed the first live agentic transaction in Singapore with DBS and UOB, where an AI agent booked and paid for a ride to Changi Airport (Mastercard, 2026). Agentic commerce redefines the merchant of record, disputes, chargebacks and even KYC, a shift that will reshape card economics within 24 months.

Trend 3: Multi-agent architectures are replacing monolithic copilots. Leading APAC banks are moving from single, general-purpose chat interfaces to specialized agent networks: a knowledge agent for policy retrieval, a data agent for query composition, an actions agent for system-of-record writes, and an orchestrator that plans across them. This model, inspired by microservices, improves accountability, testability, and cost control.

Trend 4: Responsible AI maturity is now an APAC advantage. Backbase's Banking Predictions 2026 report notes that Asia-Pacific leads globally in responsible AI maturity, driven by prescriptive supervision from MAS, HKMA and APRA. What was once viewed as a regulatory drag is emerging as a competitive moat, giving APAC banks a template to safely scale where US and European peers are still negotiating with regulators.

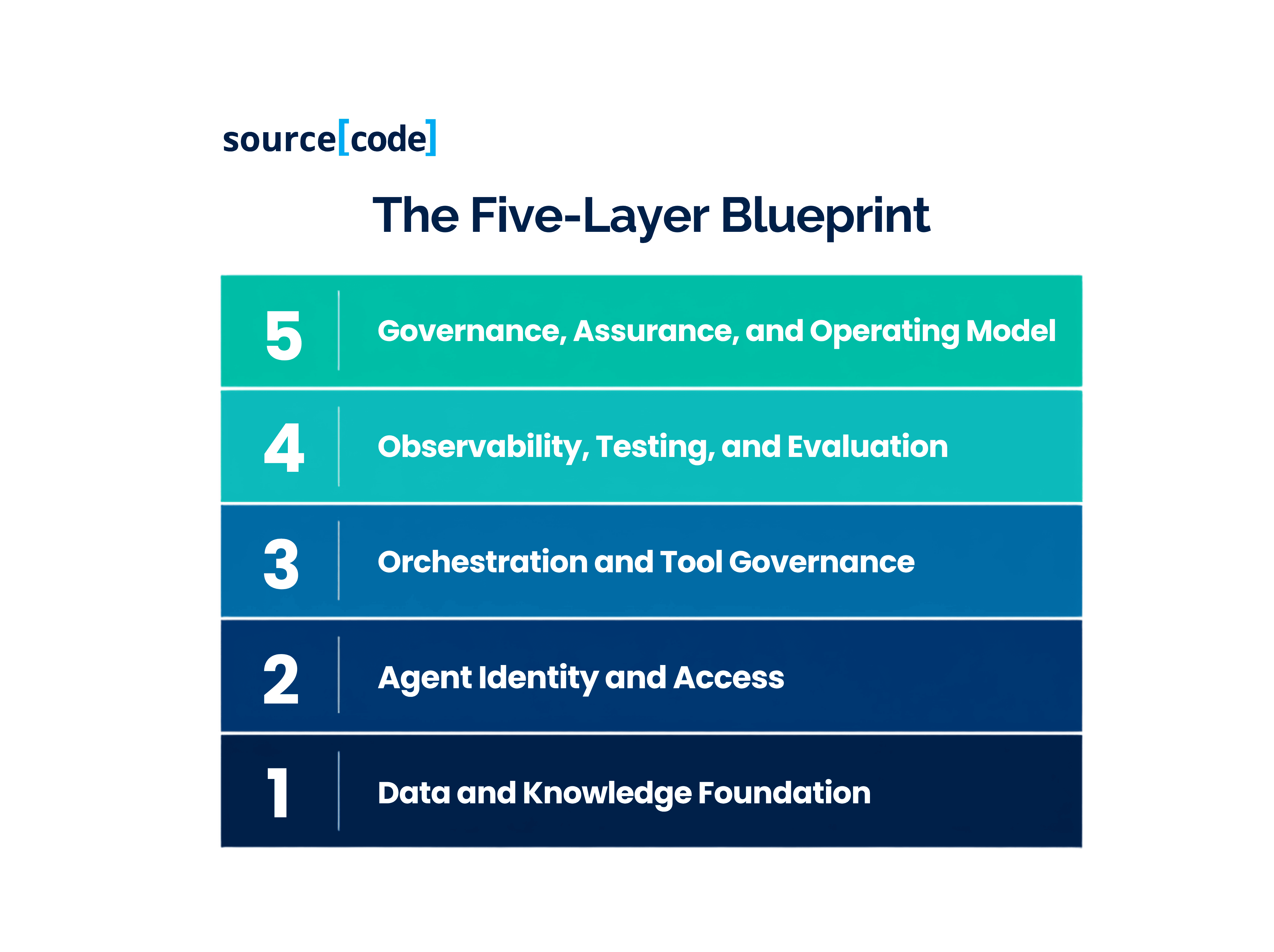

Strategic Analysis: The Five-Layer Blueprint for Production-Grade Agentic AI

Executives should evaluate their agentic AI programme against five layers. Underinvestment in any one layer is the most common cause of stalled scale-up.

Layer 1: Data and Knowledge Foundation. Agents are only as good as the data and documents they can retrieve, reason over, and act on. This layer requires a unified semantic model across customer, product, transaction and reference data; retrieval-augmented generation (RAG) pipelines with lineage and freshness guarantees; and policy-aware knowledge graphs that encode both business rules and regulatory obligations. Without it, hallucinations become inevitable and audit becomes impossible.

Layer 2: Agent Identity and Access. Every agent should hold a distinct, cryptographically verifiable identity provisioned through the bank's IAM and PAM stack. Entitlements must be just-in-time, scoped to a specific task or session, and revocable. Actions must be attributable end-to-end to both the agent and the authorizing human where consequential. This is the layer APRA has publicly flagged as inadequate across the Australian industry.

Layer 3: Orchestration and Tool Governance. A production agent programme requires a controlled catalogue of tools (APIs, functions, connectors) that agents may invoke, versioned and code signed. Orchestration engines must enforce guardrails: budget ceilings, tool-use policies, escalation to humans, and refusal patterns. Open standards such as MCP (Model Context Protocol) and A2A are emerging as the interoperability layer, but banks must not concede control of that layer to third parties.

Layer 4: Observability, Testing, and Evaluation. Traditional application performance monitoring is insufficient. Agent observability requires trace-level visibility into every reasoning step, tool call, cost and latency, plus continuous evaluation for hallucination, bias, prompt injection and data leakage. Golden datasets and adversarial red teaming should be industrialized, not artisanal.

Layer 5: Governance, Assurance, and Operating Model. This layer includes the agent control room, human override and kill-switch protocols recommended by Deloitte (2026), aligned with MAS's AI Risk Management Toolkit and APRA's expectations. It also includes the operating model changes, new roles such as agent product owner, agent SRE, and prompt engineer, and reallocation of the 93% technology / 7% people ratio identified by Deloitte.

Real-World Examples from APAC

DBS Bank (Singapore). DBS has operationalized 370-plus AI use cases, 1,500-plus models, and now attributes S$1 billion of 2025 revenue uplifting to AI (CNBC, 2025). Vertical wins include ESG questionnaire automation, documentary trade legal review, and adverse-media screening for AML/KYC. Crucially, DBS has invested heavily in a proprietary governance layer, internally described as an "AI control tower", and made explainability and human oversight non-negotiable design constraints.

UOB (Singapore). UOB partnered with Mastercard on the first live agentic transaction in Singapore, demonstrating end-to-end authenticated payments initiated by an AI agent on behalf of a customer (Mastercard, 2026). UOB's pattern, piloting agentic commerce with a regulated partner rather than in isolation, is a template APAC banks should study.

Australia's Big Four. Following APRA's April 2026 letter, all four major Australian banks committed to accelerated AI governance uplift programmes, focused on non-human identity, model risk management and independent assurance. This is likely the largest single agentic AI governance intervention in the region.

Regional Insurers. In insurance, agentic AI is being deployed for underwriting workflows, claims, triage, and fraud detection. Southeast Asian insurers are combining agentic pipelines with WhatsApp and Zalo channels, recognizing that mobile-first customers will not migrate to email or portals for claims events.

Actionable Recommendations for BFSI Executives

For CEOs and Boards. Reset the AI narrative from "productivity of individual employees" to "productivity of the operating model." Approve a dedicated agentic AI investment case with a three-year horizon, a portfolio of at most 10-15 enterprise agents, and explicit board-level KPIs on adoption, risk incidents and unit economics.

For CIOs and CTOs. Publish an internal agentic AI reference architecture that covers all five layers above. Insist on non-human identity, tool cataloguing and observability from day one. Do not permit teams to promote agents to production without cost observability at the trace level.

For CDOs and Heads of Data. Prioritize the top five data products required by the first agents and industrialize their lineage, quality and entitlement. Treat semantic modelling as a strategic asset, not a project.

For Heads of Risk and Compliance. Adopt the MAS AI Risk Management Toolkit as the internal baseline, even outside Singapore. Define escalation, override and human-in-the-loop policies before agents are deployed, not after.

For Heads of Digital and Product. Redesign customer journeys assuming that AI agents on both sides, the bank's and the customer's, will negotiate transactions. Prepare for agentic commerce disputes, consent frameworks and identity assurance patterns.

The sourceCode Perspective

sourceCode partners with banks, insurers and non-bank financial institutions across APAC to move AI programmes from experimentation to enterprise-grade production. Our engineering teams observe three recurring patterns in successful agentic AI transformations.

First, the winners treat the agent as a software product, not a science project with product owners, backlogs, SLOs, and a defined path to decommissioning. Second, they build the platform once and reuse it across the business, rather than allowing each function to procure its own agent framework. Third, they invest ahead of the curve in the "boring" foundations: identity, observability, secrets management, prompt versioning and evaluation harnesses. This is the layer where most programmes silently fail.

Our BFSI-specialized capabilities include cloud and data platform modernization, secure delivery of AI and agentic systems, engineering for regulated workloads, and independent assurance of AI governance. We work alongside internal teams to shorten time-to-value while raising the ceiling of what can be safely deployed. In the APAC context, we combine deep engineering capacity in Vietnam, Singapore and Australia with the compliance rigor BFSI clients require. More about our approach is available at sourcecode.com.au.

Conclusion

Agentic AI is not a marginal upgrade to the last generation of AI in banking; it is a re-platforming event on the scale of the shift to cloud. The distance between banks that industrialize agentic operations and those that do not will compound quickly, because agents create data, refine themselves, and lower the marginal cost of the next agent. APAC banks have three advantages the rest of the world does not: prescriptive regulators giving clear expectations, a customer base that will use agentic products enthusiastically, and a live playbook from DBS, UOB and their peers.

The window to build the operating model, not the models, is 2026. Boards that treat this as an engineering discipline, not a proof-of-concept, will define the next decade of APAC financial services.

Looking to move your agentic AI programme from pilot to enterprise-grade production? Talk with sourceCode about building the platform, governance and engineering foundations that make it safe to scale. Visit https://www.sourcecode.com.au to start the conversation.

FAQ

Q: What is the difference between generative AI and agentic AI in banking? Generative AI produces content: a summary, a draft email, a piece of code in response to a single prompt. Agentic AI plans a multi-step task, decides which tools and data to use, executes those steps, evaluates the outcome, and adapts. In banking, generative AI drafts a credit memo; agentic AI drafts the memo, retrieves the required financials, runs the covenant checks, opens the workflow ticket, and escalates exceptions.

Q: How are APAC regulators approaching agentic AI in 2026? MAS published an AI Risk Management Toolkit in early 2026 covering traditional, generative and agentic AI. APRA issued a formal industry letter in April 2026 calling for a step-change in governance, specifically citing agentic and autonomous workflows and non-human identity as concerns. HKMA has brought forward a Cyber Resilience Testing Framework and required business model reassessment.

Q: How much can agentic AI save an APAC bank? McKinsey (2026) estimates 20-30% cost reduction in operations by 2028 for banks that industrialize agentic operations. DBS attributes an incremental S$1 billion of revenue to AI in 2025. Individual use cases have delivered 60%-plus productivity gains and multi-million-dollar annual savings.

Q: Why do most agentic AI projects fail? Data readiness, non-human identity gaps, over-investment in technology relative to operating model change, and immature ROI discipline. Gartner projects that more than 40% of agentic AI projects will be cancelled by 2027 as a result.

Q: What role does sourceCode play? sourceCode helps APAC BFSI institutions design and deliver the engineering foundations for production-grade agentic AI: reference architecture, identity for agents, orchestration, observability, and independent governance assurance, combining deep regional delivery capacity with BFSI compliance rigor.

References

Australian Prudential Regulation Authority (APRA) 2026, Letter to APRA-regulated entities: managing the risks of artificial intelligence, 30 April, APRA, Sydney, viewed 7 July 2026, https://www.regulationtomorrow.com/2026/05/apra-calls-for-a-step-change-in-ai-related-risk-management-and-governance/.

Backbase 2026, Banking Predictions 2026: AI and the Future of Banking, Backbase, Amsterdam, viewed 7 July 2026, https://www.backbase.com/banking-predictions-report-2026/ai-and-the-future-of-banking.

Boston Consulting Group (BCG) 2026, How Retail Banks Can Put Agentic AI to Work, BCG, viewed 7 July 2026, https://www.bcg.com/publications/2026/how-retail-banks-can-put-agentic-ai-to-work.

Boston Consulting Group (BCG) 2026, The US$200 Billion Agentic AI Opportunity for Tech Service Providers, BCG, viewed 7 July 2026, https://www.bcg.com/publications/2026/the-200-billion-dollar-ai-opportunity-in-tech-services.

CNBC 2025, 'CEO of Southeast Asia's top bank DBS says AI adoption already paying off', CNBC, 14 November, viewed 7 July 2026, https://www.cnbc.com/2025/11/14/ceo-southeast-asias-top-bank-dbs-says-ai-adoption-already-paying-off.html.

DBS Bank 2026, DBS is first bank in Asia Pacific to pilot Visa Intelligent Commerce for everyday payments, DBS Newsroom, viewed 7 July 2026, https://www.dbs.com/newsroom/DBS_is_first_bank_in_Asia_Pacific_to_pilot_Visa_Intelligent_Commerce_for_everyday_payments.

Deloitte 2026, Managing the New Wave of Risks from AI Agents in Banking, Deloitte Insights, viewed 7 July 2026, https://www.deloitte.com/us/en/insights/industry/financial-services/agentic-ai-risks-banking.html.

Deloitte 2026, 2026 Banking and Capital Markets Outlook, Deloitte Insights, viewed 7 July 2026, https://www.deloitte.com/us/en/insights/industry/financial-services/financial-services-industry-outlooks/banking-industry-outlook.html.

Financial Stability Board (FSB) 2026, Sound Practices for Financial Institutions' Responsible AI, FSB, Basel, viewed 7 July 2026, https://www.fsb.org/uploads/P100626.pdf.

Gartner 2026, Hype Cycle for Agentic AI 2026, Gartner Research, viewed 7 July 2026, https://www.gartner.com/en/articles/hype-cycle-for-agentic-ai.

Hong Kong Monetary Authority (HKMA) 2026, Circular on business model reassessment and AI-driven cyber threats, HKMA, Hong Kong, viewed 7 July 2026, https://kpmg.com/cn/en/insights/2026/06/hong-kong-banking-report-2026/cyber-security.html.

Mastercard 2026, Mastercard delivers its first live agentic transaction in Singapore with DBS and UOB, Mastercard Newsroom, viewed 7 July 2026, https://www.mastercard.com/news/ap/en/newsroom/press-releases/en/2026/mastercard-delivers-its-first-live-agentic-transaction-in-singapore-with-dbs-and-uob/.

Mayer Brown 2026, AI Regulation in Singapore and Hong Kong: A Mid-Year Checkpoint, July, viewed 7 July 2026, https://www.mayerbrown.com/en/insights/publications/2026/07/ai-regulation-in-singapore-and-hong-kong-a-mid-year-checkpoint.

McKinsey & Company 2026, AI in Asia: Reimagining Banking Operations through Agentic AI, McKinsey Operations Practice, viewed 7 July 2026, https://www.mckinsey.com/capabilities/operations/our-insights/ai-in-asia-reimagining-banking-operations-through-agentic-ai.

McKinsey & Company 2026, The Paradigm Shift: How Agentic AI Is Redefining Banking Operations, McKinsey Operations Practice, viewed 7 July 2026, https://www.mckinsey.com/capabilities/operations/our-insights/the-paradigm-shift-how-agentic-ai-is-redefining-banking-operations.

McKinsey & Company 2026, State of AI Trust in 2026: Shifting to the Agentic Era, McKinsey Tech Forward, viewed 7 July 2026, https://www.mckinsey.com/capabilities/tech-and-ai/our-insights/tech-forward/state-of-ai-trust-in-2026-shifting-to-the-agentic-era.

Monetary Authority of Singapore (MAS) 2026, Project MindForge Phase 2: AI Risk Management Toolkit for Financial Services, MAS, Singapore, viewed 7 July 2026, https://www.mas.gov.sg/.