The Fraud Reckoning: Rewiring APAC Banking and Insurance Defenses for Deepfakes, Synthetic Identity and Agentic AI Attacks

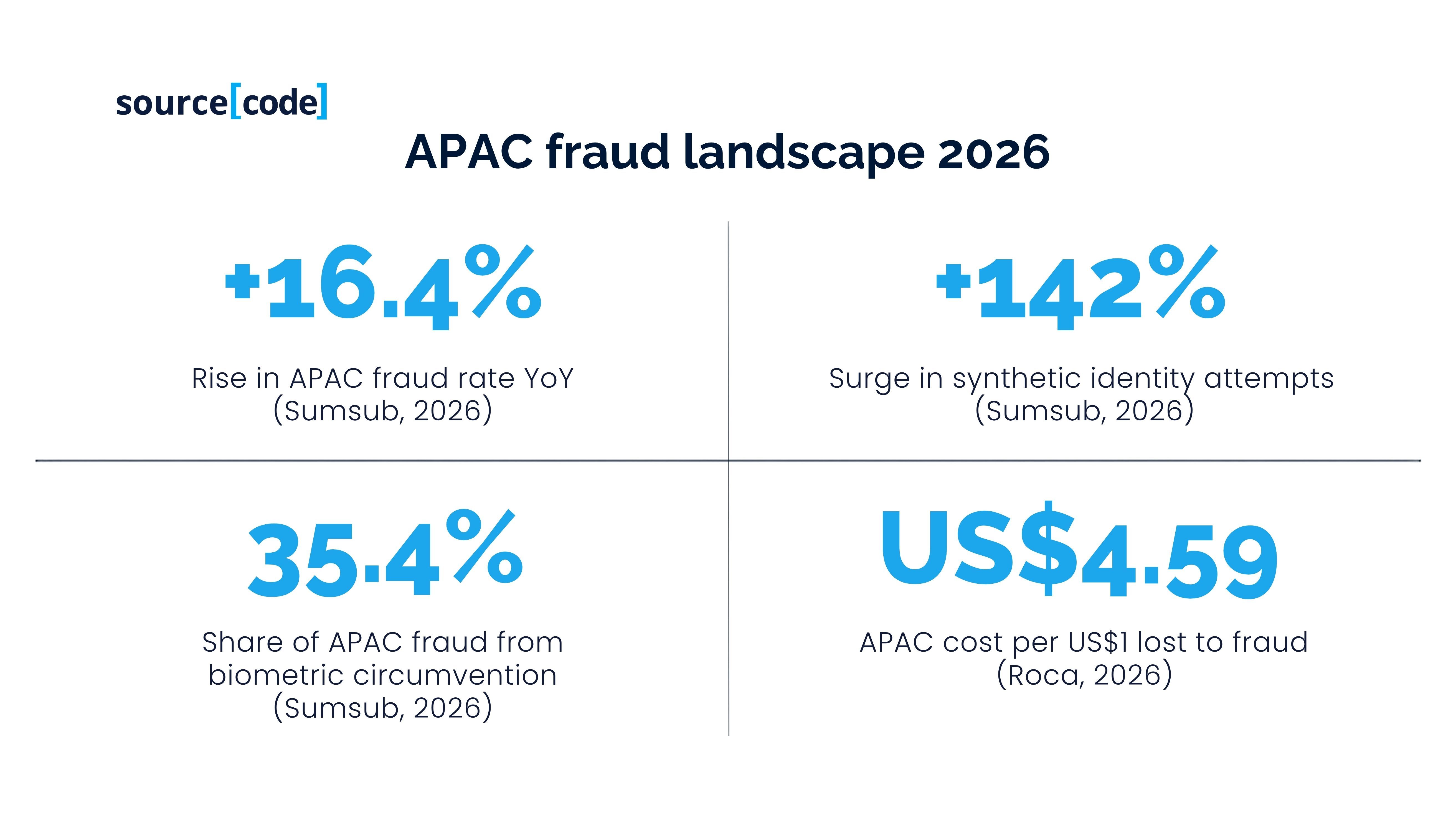

In 2026, fraud in Asia-Pacific has stopped behaving like an operational nuisance and started behaving like a systemic risk. Sumsub's APAC Fraud in 2026 report records a 16.4% year-on-year rise in the regional fraud rate, even as fraud declined in other regions, and a 142% surge in synthetic identity attacks (Sumsub, 2026). Biometric circumvention, where a selfie fails to match submitted identification, now accounts for 35.4% of all fraudulent activity across APAC (Sumsub, 2026). At a global level, deepfake-related fraud losses exceeded US$410 million in the first half of 2025 alone (Bright Defense, 2026), and the volume of files created with deepfake technology grew from roughly 500,000 in 2023 to about 8 million in 2025 (Keepnet Labs, 2026).

For APAC banks and insurers, the economics are especially punishing. Recent industry benchmarks put fraud remediation cost at US$4.59 for every US$1 lost, materially higher than in the United States or Europe (Roca, 2026). BCG has warned that agentic AI will "industrialize" scams, compressing attack cycles, and personalizing social engineering at scale (BCG, 2026). Regulators have moved into step: the Hong Kong Monetary Authority (HKMA) launched an AI-led anti-fraud campaign in 2026 (HKMA, 2026); the Monetary Authority of Singapore (MAS) formalized its AI Risk Management Guidelines in 2025 (MAS, 2025); and the Australian Prudential Regulation Authority (APRA) issued an industry letter in April 2026 warning that AI governance is not keeping pace with adoption, including in fraud and scam disruption (APRA, 2026).

For APAC banks and insurers, the economics are especially punishing. Recent industry benchmarks put fraud remediation cost at US$4.59 for every US$1 lost, materially higher than in the United States or Europe (Roca, 2026). BCG has warned that agentic AI will "industrialize" scams, compressing attack cycles, and personalizing social engineering at scale (BCG, 2026). Regulators have moved into step: the Hong Kong Monetary Authority (HKMA) launched an AI-led anti-fraud campaign in 2026 (HKMA, 2026); the Monetary Authority of Singapore (MAS) formalized its AI Risk Management Guidelines in 2025 (MAS, 2025); and the Australian Prudential Regulation Authority (APRA) issued an industry letter in April 2026 warning that AI governance is not keeping pace with adoption, including in fraud and scam disruption (APRA, 2026).

This article sets out a five-part blueprint for how APAC banks, insurers, financial-services, and fintech firms should rebuild fraud and financial-crime defenses for the age of deepfakes, synthetic identity, and agentic AI. The central argument: the winning institutions will not be those that buy the most fraud-tech tools, but those that industrialize a real-time, AI-native, cross-domain defense stack with governance, identity, and human-in-the-loop controls treated as first-class engineering disciplines.

Fraud in APAC Has Turned Systemic

For most of the last decade, fraud loss ratios in APAC banking behaved much like their global peers: an unpleasant but manageable line item on the risk report. Three shifts have changed that picture in 2026.

First, the attackers have industrialized. Sumsub's Identity Fraud Report 2025-2026 documents fraud shifting from isolated attempts to complex multi-step schemes coordinated across mule networks, deepfake providers, and social-engineering rings (Sumsub, 2026). The same report projects a further surge in agentic AI-driven scams in 2026 as attackers' pair large language models with orchestration frameworks that can execute end-to-end attack chains, from lure to impersonation to money movement without human touch.

Second, deepfakes have moved from novelty to commodity. Bright Defense's 2026 benchmarking study estimates that deepfakes now sit behind roughly 11% of global fraud, up from a negligible share three years ago (Bright Defense, 2026). Keepnet Labs (2026) tracks a 16-fold increase in deepfake file creation between 2023 and 2025. Within APAC, Sumsub reports Vietnam (25.3%) and Japan (23.4%) as the two largest sources of detected deepfake incidents - a distribution that reflects both attacker geography and target density (Sumsub, 2026).

Third, synthetic identity has become the region's defining fraud vector. Datos Insights and Mitek concluded in June 2026 that synthetic identity is now "the defining fraud threat of 2026" globally, and the pattern is unusually acute in APAC, where digital onboarding volumes are high and identity ecosystems are fragmented (Businesswire, 2026). Sumsub's regional data shows synthetic identity attempts up 142% year-on-year across APAC (Sumsub, 2026). The combination of AI-fabricated documents, deepfake liveness bypass, and rented mule accounts creates identities that are, in the auditor's phrase, "true enough" to survive traditional KYC.

The macroeconomic backdrop compounds the problem. Cross-border real-time payment corridors are expanding through initiatives such as Project Nexus (BIS, 2025), embedded finance is pushing new customer flows into non-bank platforms, and Southeast Asia's under-banked adult population, still more than 70% in some markets according to World Bank (2024) estimates, is coming online at pace. Every one of these is a growth engine for banks and insurers; every one of them is also a new attack surface.

The Economics of Losing the Fraud War

The financial impact of this shift is now visible on the P&L. Juniper Research forecasts global online payment fraud losses will exceed US$362 billion between 2023 and 2028 (Juniper, 2024). Deloitte projects that generative AI could enable fraud losses to reach US$40 billion in the United States alone by 2027, up from US$12.3 billion in 2023, a 32% compound annual growth rate (Deloitte, 2024). For APAC, conservative industry estimates of sourced fraud losses across banking range between US$7.5 billion and US$16 billion annually (Roca, 2026).

Two things make this economics particularly hostile for APAC institutions.

First, the cost-to-loss ratio. Where US and European banks typically spend under US$4 for every US$1 of fraud loss, APAC institutions are averaging US$4.59, reflecting the double burden of higher attack volumes and less-mature detection stacks (Roca, 2026). The delta is a direct tax on cost-income ratios that are already under pressure from rate normalization and digital-native competition.

Second, the shift of liability. Australia's Scams Prevention Framework (Treasury, 2025), Singapore's Shared Responsibility Framework (MAS, 2024), and comparable moves in Hong Kong and the UK are re-allocating fraud losses to banks and telecoms where controls are judged insufficient. What used to be a customer-borne loss is becoming a bank-borne loss. Institutions that cannot demonstrate proportionate defenses will absorb the delta.

Sitting alongside the losses is a rising defensive investment. Juniper Research projects AI-driven fraud detection will save banks more than £9.6 billion annually by 2026, with leading institutions reporting detection accuracy above 90% for well-tuned models (Juniper, 2024). But the gains accrue disproportionately to institutions that operate as one platform, not as a portfolio of siloed rules engines glued together across product lines.

Four Attack Vectors Executives Must Understand

To make budget decisions coherently, executives need to understand which threats they are actually funding against. Four vectors dominate the 2026 threat landscape.

Deepfake-enabled authorized push payment (APP) scams. Voice cloning of executives, celebrity endorsements, and family-member impersonations are compressing the time-to-conviction in social-engineering attacks. Hong Kong's landmark 2024 deepfake video call, in which a finance employee was tricked into transferring US$25 million by a live deepfake of the CFO (SCMP, 2024), remains the reference case but incident frequency has since moved into the double digits per quarter across major APAC banks. Detection now requires liveness, behavioral biometrics, and out-of-band verification at the transaction layer, not just at onboarding.

Synthetic identity onboarding at scale. Attackers combine real seed data (often from prior breaches), AI-generated selfies, and forged government-issued documents to construct identities that pass KYC. Sumsub reports biometric circumvention as the single largest fraud category across APAC at 35.4% of all cases (Sumsub, 2026). The synthetic identities are then "aged" through low-value transactions before being weaponized for credit fraud, mule accounts, or claims fraud in insurance.

Agentic AI attack orchestration. BCG's May 2026 analysis warns that agentic systems will "industrialize" scams by chaining lure generation, victim research, personalized social engineering, and money movement into a single autonomous workflow (BCG, 2026). The economic effect is a step-change reduction in cost per attempt: the marginal cost of a personalized scam approaches zero, and attack volume scales accordingly. Sumsub predicts agentic scams will be the defining fraud pattern of 2026 (Sumsub, 2026).

Claims and underwriting fraud in insurance. Aviva's public description of its rewired claims journey demonstrated that AI could strip £60 million in annual leakage from a single carrier (McKinsey, 2025). The same technology in attackers' hands is producing fabricated accident photos, synthetic medical records, and AI-generated repair invoices at scale. Insurers that cannot verify the provenance of evidence in claims will pay for both the fraud and the settlement cost.

The Regulatory Perimeter Is Closing - Fast

APAC regulators have moved from principle-setting to expectation-setting in a matter of months.

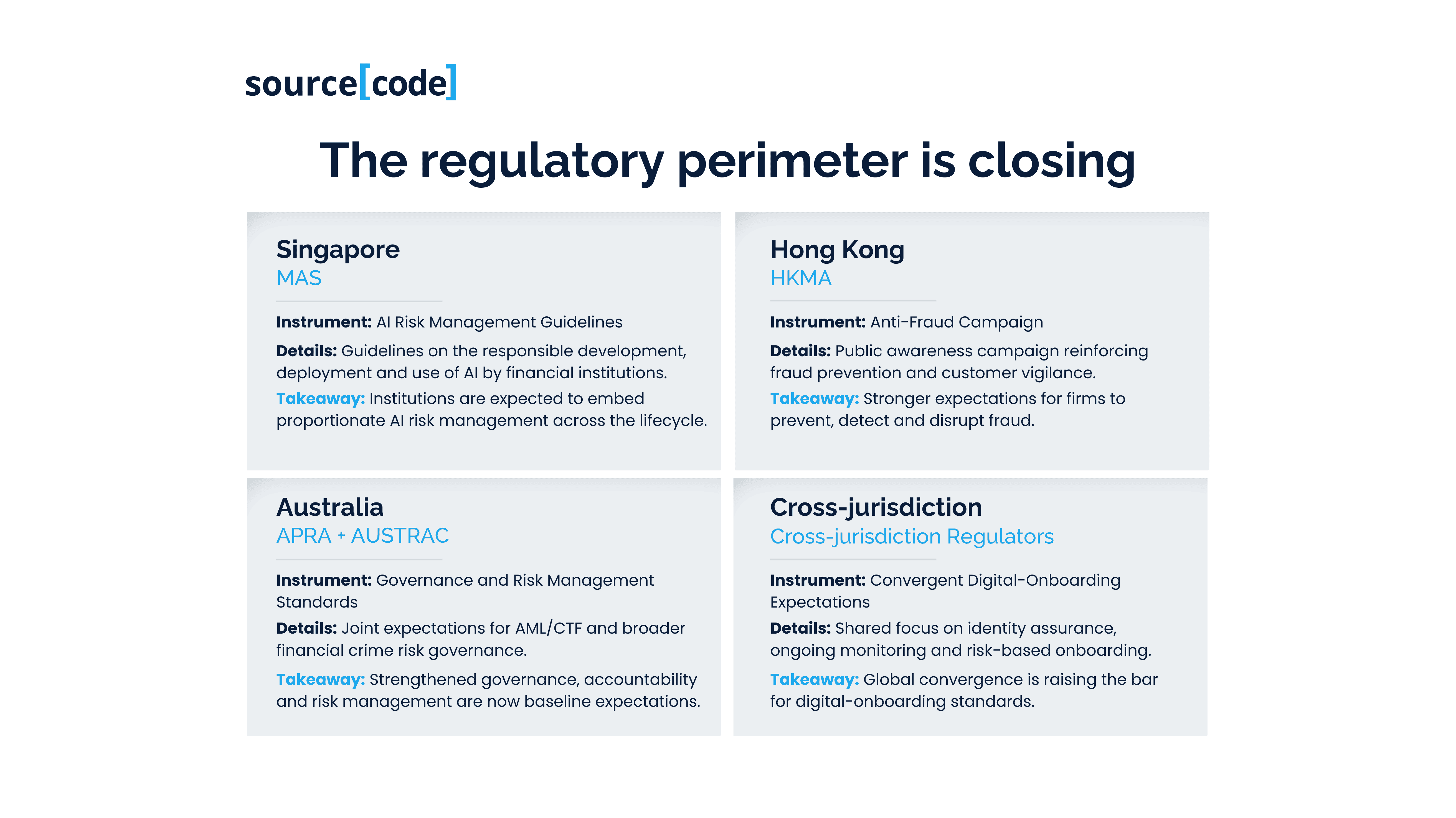

Singapore (MAS). The 2018 FEAT principles, the 2024 information paper on AI model risk management, and the 2025 Guidelines on AI Risk Management have collectively established that AI systems used in fraud detection and financial crime are subject to the same governance, explainability, and accountability standards as any other material model (MAS, 2025). MAS's Shared Responsibility Framework has further raised the bar on real-time scam detection and pre-transaction controls (MAS, 2024).

Singapore (MAS). The 2018 FEAT principles, the 2024 information paper on AI model risk management, and the 2025 Guidelines on AI Risk Management have collectively established that AI systems used in fraud detection and financial crime are subject to the same governance, explainability, and accountability standards as any other material model (MAS, 2025). MAS's Shared Responsibility Framework has further raised the bar on real-time scam detection and pre-transaction controls (MAS, 2024).

Hong Kong (HKMA). The HKMA's 2024 white paper Reshaping Banking with Artificial Intelligence set out expectations on AI adoption; the 2026 anti-fraud campaign has translated those into operational action, with the HKMA partnering with Hong Kong Police, the Hong Kong Association of Banks, and the Privacy Commissioner's office to expand Scameter - a real-time database of suspicious accounts and phone numbers, and to run thematic reviews of banks' anti-fraud systems (HKMA, 2026).

Australia (APRA and AUSTRAC). APRA's 30 April 2026 letter to industry stated bluntly that AI governance "has not matured at the same pace" as AI adoption and specifically named customer-facing fraud and scam disruption as a supervisory concern (APRA, 2026). CPS 230 obligations on operational risk, and CPS 234 on information security, remain the underlying instruments. AUSTRAC's 2026 priorities continue to focus on suspicious matter reports (SMRs) generated by real-time monitoring rather than end-of-day batch.

Cross-jurisdiction convergence. The FCA, MAS, HKMA, APRA and AUSTRAC have all issued commentary on digital onboarding expectations, stressing that biometric checks, document verification and ongoing monitoring must operate as an integrated stack rather than in isolation (Trustsphere, 2026). BIS and FSB have amplified these themes at the global level (BIS, 2025). The direction of travel is unambiguous: real-time, integrated, explainable, and evidenced.

A Five-Part Blueprint for a 2026-Ready Defense Stack

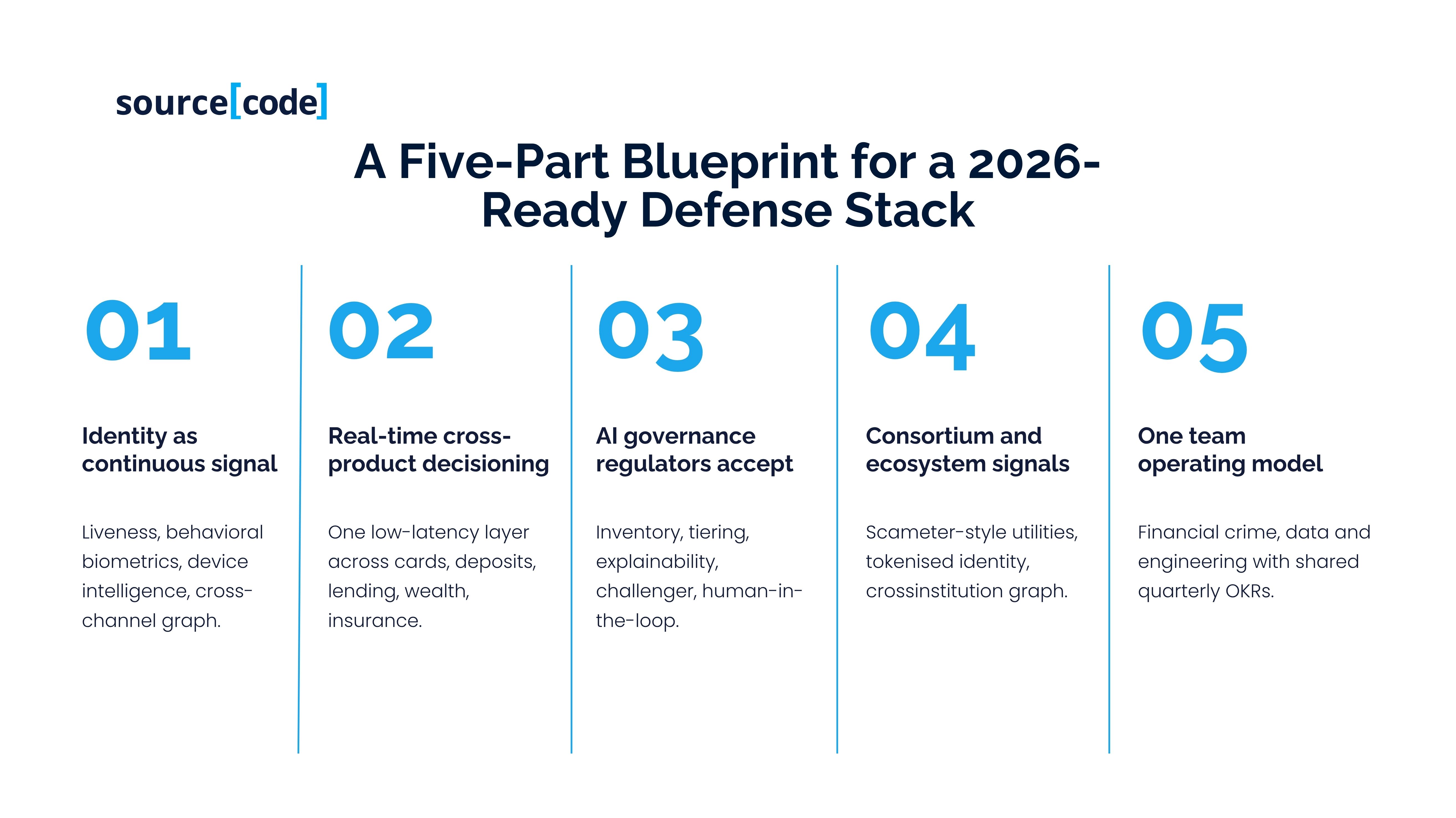

The strategic question is no longer whether to invest in AI-native fraud defense; it is which parts of the stack to industrialize first, and in what sequence. sourceCode's engagement pattern across BFSI clients points to a five-part blueprint that leadership teams can use to sequence investment.

Identity as a Continuous Signal, not a One-Time Event

Traditional KYC treats identity as verified once at onboarding. The 2026 threat surface demands that identity be treated as a continuous signal: liveness re-checks at high-risk transactions, behavioral biometrics on every session, device intelligence at every interaction, and cross-channel graph analytics that link the digital, telephony and branch estates. This is the single largest capability gap sourceCode observes across mid-tier APAC banks and insurers.

Executive question: Can your organization answer, in real time, whether the person interacting with your channel is (a) the customer, (b) authorized by the customer, or (c) neither?

A Real-Time, Cross-Product Decisioning Layer

Fraud, AML, sanctions, credit and marketing decisions still run on separate rules engines in most APAC banks. Attackers exploit exactly those seams. The winning architecture is a single low-latency decisioning layer that fuses fraud signals across cards, deposits, lending, wealth and insurance, invoked in-line during the transaction, not offline overnight. This is where feature stores, streaming platforms, and model-serving infrastructure become financial-crime infrastructure.

Executive question: What is your median decision latency at the transaction layer, and how does it compare with your peer set?

AI Governance That Auditors and Supervisors Will Accept

Deploying models faster than you can govern them is the failure mode APRA has named explicitly (APRA, 2026). The governance stack that regulators want to see comprises: a model inventory covering every AI system in the fraud path; documented risk tiering with proportionate controls; explainability instrumentation; challenger models and shadow deployments; and clear ownership of the human-in-the-loop path. MAS's 2025 guidelines and HKMA's expectations converge on the same architecture (MAS, 2025; HKMA, 2024).

Executive question: Could you produce, within 24 hours, a full inventory and risk-tiering of every AI model touching your fraud, AML or KYC pipeline?

Consortium and Ecosystem Signals

No single institution has enough data to detect coordinated attacks at the pace attackers now operate. HKMA's Scameter and MAS-led information-sharing initiatives are the direction of travel: consortium data, tokenized identity signals, and cross-institution graph analytics that surface mule networks and coordinated onboarding attempts (HKMA, 2026). Institutions that architect for consortium participation early, with the privacy engineering and data contracts to make it safe will have a compounding advantage.

Executive question: What signals do you contribute to and receive from industry consortia today, and what is your roadmap to expand that footprint?

An Operating Model Where Engineering and Financial Crime Are One Team

The final and most often overlooked lever is organizational. Banks and insurers that treat financial crime as a compliance-run function, with engineering as a supplier, consistently fall behind. The institutions moving fastest - DBS in Singapore, Commonwealth Bank in Australia, several tier-one Japanese banks, have fused financial crime, data, and engineering into a single product-oriented operating model with shared OKRs. This is a leadership decision, not a technology decision.

Executive question: Do your Chief Risk, Chief Data, and Chief Technology Officers share a common set of quarterly outcomes on financial crime, or do they optimize separately?

Real-World Signals from the APAC Front Line

Several APAC institutions have already begun to industrialize elements of this blueprint. DBS Bank in Singapore now runs more than 370 AI use cases against 1,500-plus models, contributing an incremental S$1 billion in 2025 revenue and materially strengthening its fraud posture (CNBC, 2025). Hong Kong's regulators, together with the banking association, have expanded Scameter into a real-time fraud-signals utility that banks integrate directly with transaction monitoring (HKMA, 2026). In Australia, the Big Four have collectively invested more than A$1 billion in scam-defense capability over 2024-2025 under the Scams-Safe Accord (ABA, 2025). In insurance, Aviva's rewired claims journey, developed with QuantumBlack and Orphoz, has deployed 80-plus production models and delivered £60 million in annual savings and a two-thirds reduction in customer complaints (McKinsey, 2025).

The through-line is consistent: institutions that treat fraud defense as an engineered platform with governance built in, not as a portfolio of point solutions capture the returns.

The sourceCode Perspective

Across BFSI engagements in APAC, sourceCode observes three consistent inflection points where organizations either accelerate or stall.

The first is architectural. Institutions that persist with siloed fraud, AML, credit and marketing decisioning cannot compress detection latency below what modern attackers require. sourceCode's data and platform engineering practice focuses on the streaming, feature-store and model-serving infrastructure that makes an integrated real-time decisioning layer economically viable at scale.

The second is governance. Model risk management, explainability, and human-in-the-loop design are treated in many institutions as documentation exercises after the fact. sourceCode's AI governance and MLOps engagements embed these as pipeline artefacts: model cards, lineage, challenger frameworks, and observability, so that supervisors and internal auditors can see the evidence in the tooling itself.

The third is the operating model. The most successful transformations pair engineering delivery with a redesign of how financial crime, data and technology teams work together. sourceCode's role is not to replace client teams, but to accelerate their capability build through embedded pods, platform enablement, and executive coaching, until the client operates the platform independently.

The framing sourceCode brings to boards and executive committees is that fraud defense in 2026 is a capital allocation question first and a technology question second. The institutions that will emerge with structural advantage are the ones that treat their financial-crime platform as core infrastructure, funded and governed accordingly.

Conclusion: The Window Is Narrower Than It Looks

Fraud in APAC has crossed a threshold. Synthetic identity is systemic. Deepfakes are commodity. Agentic AI attackers are compressing the cost per attempt toward zero. Regulators have moved from principles to expectations. Liability is shifting toward banks and insurers. And the institutions that are moving fastest are already establishing platform advantages that will be difficult to close.

The remedy is not more point tools. It is an engineered defense stack: identity as a continuous signal, a real-time cross-product decisioning layer, AI governance regulators will accept, consortium signals plugged in early, and an operating model that makes engineering and financial crime one team. Institutions that make these choices in the next 12-18 months will define the fraud economics of the second half of the decade.

Looking to explore how your organization can rewire its fraud, AML and financial-crime platform for the deepfake era while meeting the expectations of MAS, HKMA, APRA and AUSTRAC? Talk with sourceCode about building the identity, decisioning and governance capabilities that turn financial-crime defense into a durable engineering advantage.

Learn more at www.sourcecode.com.au.

Frequently Asked Questions (FAQs)

Q: What is the single biggest fraud threat facing APAC banks in 2026? A: Synthetic identity fraud, which has grown 142% year-on-year across APAC, is the fastest-growing systemic threat. When combined with deepfake liveness bypass and mule-account networks, it undermines the assumption that a customer verified at onboarding remains verifiable in subsequent interactions (Sumsub, 2026).

Q: How much do APAC banks lose to fraud each year? A: Conservative industry estimates put sourced fraud losses across APAC banking between US$7.5 billion and US$16 billion annually. APAC institutions also spend US$4.59 for every US$1 of fraud lost - materially higher than in the US or Europe (Roca, 2026).

Q: What does APRA expect Australian banks and insurers to do about AI-driven fraud? A: APRA's April 2026 letter directs regulated entities to ensure that AI governance keeps pace with AI adoption, including in customer-facing fraud and scam disruption. Existing prudential standards (CPS 230 operational risk, CPS 234 information security) apply to AI systems (APRA, 2026).

Q: How is agentic AI changing fraud economics? A: Agentic AI drives the marginal cost of a personalized scam toward zero, allowing attackers to scale volume without proportional cost. BCG (2026) argues this will "industrialize" scams; Sumsub (2026) forecasts agentic scams as the defining fraud pattern of 2026.

Q: What is the first investment executives should sequence? A: Identity as a continuous signal - liveness re-checks at high-risk transactions, behavioral biometrics per session, device intelligence, and cross-channel graph analytics. It is the largest capability gap sourceCode observes in the mid-tier APAC market and the foundation for every other layer.

Reference

Australian Banking Association (ABA). (2025). Scams-Safe Accord Progress Update. Sydney: ABA.

Australian Prudential Regulation Authority (APRA). (2026). Letter to Industry on Artificial Intelligence. 30 April 2026. Sydney: APRA. Available at: https://www.apra.gov.au/apra-letter-to-industry-on-artificial-intelligence-ai

Bank for International Settlements (BIS). (2025). Project Nexus: Enabling Instant Cross-Border Payments. Basel: BIS.

BCG. (2026). Agentic AI Will Industrialize Financial Scams. Are Banks Ready? Boston: BCG. Available at: https://www.bcg.com/publications/2026/how-agentic-ai-will-industrialize-financial-scams

Bright Defense. (2026). 150+ Deepfake Statistics - March 2026. Available at: https://www.brightdefense.com/resources/deepfake-statistics/

Businesswire. (2026). Mitek and Datos Insights Report Finds Synthetic Identity Fraud Is Emerging as the Defining Fraud Threat of 2026. 10 June 2026. Available at: https://www.businesswire.com/news/home/20260610637404/en

CNBC. (2025). How DBS Bank Scaled AI to 370 Use Cases. Singapore: CNBC.

Deloitte. (2024). Generative AI Is Expected to Magnify the Risk of Deepfakes and Other Fraud in Banking. New York: Deloitte Center for Financial Services.

Hong Kong Monetary Authority (HKMA). (2024). Reshaping Banking with Artificial Intelligence. Hong Kong: HKMA.

Hong Kong Monetary Authority (HKMA). (2026). HKMA Deploys AI in 2026 Anti-Fraud Push Targeting Digital Payments. Hong Kong: HKMA.

Juniper Research. (2024). AI-Powered Fraud Detection in Banking: Global Forecasts 2024-2028. Basingstoke: Juniper Research.

Keepnet Labs. (2026). Deepfake Statistics 2026: Verified Benchmarks & Risks. Available at: https://keepnetlabs.com/blog/deepfake-statistics-and-trends

McKinsey & Company. (2025). Rewiring the Insurance Claims Journey with AI: The Aviva Case. New York: McKinsey Global Institute.

Monetary Authority of Singapore (MAS). (2024). Shared Responsibility Framework for Digital Scams. Singapore: MAS.

Monetary Authority of Singapore (MAS). (2025). Guidelines on Artificial Intelligence Risk Management. Singapore: MAS.

Roca, J. (2026). APAC Decision Intelligence: Why Banks Pay $4.59 Per Dollar Lost Without AI Detection. Available at: https://jamesroca.com/insights/apac_decision_intelligence_p1/

South China Morning Post (SCMP). (2024). Hong Kong Firm Loses HK$200 Million to Deepfake Video-Call Scam. Hong Kong: SCMP.

Sumsub. (2026). APAC Fraud in 2026. Available at: https://sumsub.com/blog/guides-reports/apac-fraud-in-2026/

Sumsub. (2026). Identity Fraud Report 2025-2026. Available at: https://sumsub.com/blog/guides-reports/identity-fraud-report-2025-2026/

Trustsphere. (2026). When Digital Onboarding Breaks: Anatomy of a KYC Failure. Available at: https://www.trustsphere.ai/post/when-digital-onboarding-breaks-anatomy-of-a-kyc-failure-and-what-supervisors-want-to-see-next

World Bank. (2024). Global Findex Database: Financial Inclusion in Southeast Asia. Washington DC: World Bank.